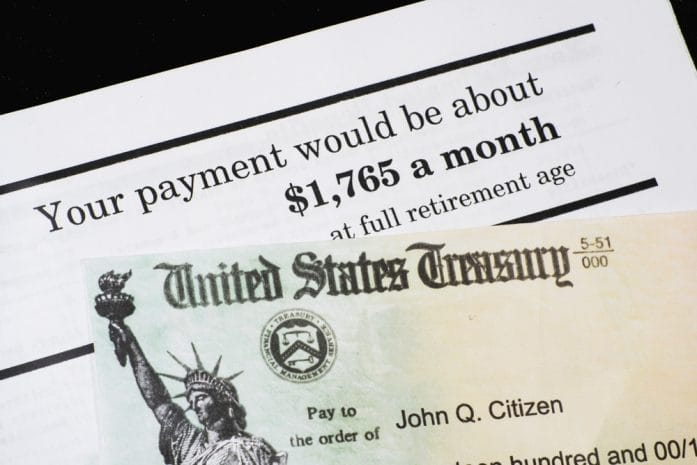

Seniors born between the 21 and 31 of the month may wait a while for May Social Security checks – Shutterstock

Social Security payments follow a structured schedule that often surprises retirees who expect all deposits to arrive on the same day. The Social Security Administration (SSA) uses birth dates to stagger payments across the month, which means timing can vary widely depending on when someone was born. Seniors with birthdays falling between the 21st and 31st of the month usually receive their payments last in the cycle. That timing becomes especially noticeable in May, when bills, medical costs, and seasonal expenses often compete for attention. Knowing where a birthday falls in the payment lineup helps retirees plan with more confidence and fewer surprises.

This schedule does not delay benefits in a harmful way, but it does create a predictable waiting pattern that affects budgeting habits. Many retirees rely heavily on Social Security as a primary income source, so even a few extra days can feel significant. The SSA designed this system to keep payments organized and reduce strain on processing systems. Still, the “late-month group” often experiences the longest gap between paychecks. That gap makes timing awareness a powerful tool for financial planning.

Why Late-Month Birthdays Land at the End of the Payment Line

The SSA assigns payment dates based on the beneficiary’s birth date to distribute deposits evenly throughout the month. This structure prevents banking congestion and helps ensure smooth processing for millions of recipients. People born between the 21st and 31st fall into the final group of the schedule, which naturally places them at the end of the cycle. That placement does not change based on income level or benefit size, so the rule applies universally. In May, this means these retirees often wait longer than peers born earlier in the month.

This system creates a predictable rhythm that repeats every month, not just in May. Seniors in the late-month group can expect their payments after the middle and early groups receive theirs. The consistency helps the SSA manage large-scale distribution efficiently across the country. However, it also means these retirees often experience the longest gap between their Social Security deposit and other income sources. That timing difference makes planning ahead especially important for households relying heavily on fixed income.

The May Social Security Payment Schedule Explained Clearly

May follows the same general SSA schedule used throughout the year, which organizes payments into three main Wednesday groups. The first group typically receives payments on the second Wednesday of the month, followed by the second group on the third Wednesday, and the final group on the fourth Wednesday. Seniors born between the 21st and 31st fall into that last Wednesday category, which often lands near the end of the month. This structure creates a clear but staggered flow of deposits across May. The system keeps operations efficient, but it also creates noticeable timing differences between groups.

The schedule becomes even more important when bills cluster at the beginning of the month. Rent, utilities, and medical costs often do not align with SSA timing, which can create short-term cash flow pressure. Seniors in the late-month group often need to stretch funds longer than others before the next deposit arrives. That gap can feel tighter in May due to seasonal expenses like travel, home maintenance, or healthcare appointments. Knowing the exact payment week helps reduce stress and improves financial stability.

Why SSA Uses Birth Dates Instead of a Single Payment Day

The SSA uses birth dates to spread out payments and avoid overwhelming financial systems with a single massive deposit day. Millions of transactions processed at once could slow down banking systems and increase the risk of errors. By dividing recipients into groups, the SSA ensures smoother and more reliable payment distribution. This method also helps banks manage incoming deposits without delays or system strain. The structure reflects a long-standing approach designed for efficiency and stability.

The birth-date grouping also helps beneficiaries receive payments in a more predictable pattern over time. Instead of one universal payday, retirees can anticipate their specific week each month. That predictability allows for better planning of recurring expenses like rent, prescriptions, and groceries. However, it also creates variation in waiting time between groups, especially for those in the final bracket. Seniors born late in the month consistently experience the longest wait, even though the system treats all groups equally.

Smart Budget Moves for Those Waiting Longer in May

Seniors in the 21st–31st birthday group often benefit from planning budgets around the latest possible payment date. That strategy prevents shortfalls during the final stretch before deposits arrive. Setting aside a small emergency buffer from earlier months can help smooth out timing gaps. Even a modest cushion reduces stress when bills come due before the SSA payment lands. This approach strengthens financial stability without requiring major lifestyle changes.

Another helpful strategy involves aligning bill due dates with known payment timing whenever possible. Some utility companies and service providers allow due date adjustments upon request. Organizing expenses around the SSA schedule can help reduce end-of-month pressure. Seniors may also benefit from tracking spending more closely during the final week before payment arrives. Small adjustments like these can make the waiting period far more manageable.

Seniors budget around their Social Security checks, so they don’t want to wait – Shutterstock

What the Late-Month Wait Really Means for May Payments

The late-month payment group does not receive reduced benefits or delayed processing errors, even though the wait feels longer. The timing difference simply reflects how the SSA distributes payments across the calendar. Seniors born between the 21st and 31st consistently receive their deposits in the final Wednesday group each month. That pattern remains stable in May and throughout the year. Predictability, not variation, defines this system.

The real impact shows up in how retirees plan their monthly cash flow around that timing. Those who prepare for the later deposit date often avoid unnecessary stress and last-minute financial strain. Awareness of the schedule turns uncertainty into routine planning. May becomes easier to navigate when expectations match the SSA structure. That clarity helps retirees stay financially steady even during longer wait periods.

Late-Month Birthdays, Longer Waits, and Smarter Planning Ahead

The SSA payment system rewards awareness more than speed, especially for seniors born between the 21st and 31st. Those retirees consistently land in the final payment wave, which creates a longer gap between deposits. May highlights that timing pattern clearly, especially when expenses stack up early in the month. Planning around the schedule helps transform that delay into a manageable routine instead of a financial stress point. Understanding the structure gives retirees a stronger sense of control over their monthly income flow.

What strategies help make the Social Security wait easier to manage each month? Share thoughts and experiences in the comments below.

Brandon Marcus is a writer who has been sharing the written word since a very young age. His interests include sports, history, pop culture, and so much more. When he isn’t writing, he spends his time jogging, drinking coffee, or attempting to read a long book he may never complete.

Medicare premiums are going up (again), and it could eat up a ton of your COLA boost – Shutterstock

Social Security recipients usually wait for the annual cost-of-living adjustment with the same excitement sports fans reserve for playoff season, because every extra dollar matters when grocery prices, utility bills, and insurance costs refuse to settle down. Early projections for the 2026 COLA point toward a modest increase, yet many retirees could watch a painful chunk disappear before the money even lands in their bank accounts. Medicare Part B premiums continue climbing at a pace that frustrates seniors who already juggle higher prescription prices, rising housing costs, and stubborn inflation at the checkout line.

Financial planners now warn that some retirees may lose nearly one-third of their COLA boost to healthcare premiums alone. That reality turns what should feel like a financial win into another year of careful budgeting and uncomfortable trade-offs.

Why Medicare Premiums Keep Climbing Faster Than Retirees Expect

Healthcare costs continue rising across nearly every corner of the economy, and Medicare absorbs much of that pressure through higher premiums, deductibles, and out-of-pocket expenses. Hospital services, specialist visits, outpatient care, and expensive prescription drugs all push program costs upward year after year. Medicare Part B premiums typically increase whenever the government projects larger spending demands for physician services and outpatient treatments. Retirees often assume their COLA increase will create breathing room, yet healthcare inflation regularly moves faster than standard consumer inflation. That mismatch leaves many seniors feeling like they run on a treadmill that keeps speeding up no matter how carefully they budget.

Some retirees remember years when Social Security increases barely covered the cost of a few extra grocery trips, while Medicare deductions quietly erased much of the benefit. In 2024, the standard Medicare Part B premium reached $174.70 per month, and analysts expect another increase for 2026 as healthcare spending continues climbing. Seniors with higher incomes face even steeper monthly costs through income-related adjustment surcharges that can dramatically raise premium totals. Financial advisors frequently point out that healthcare now represents one of the biggest ongoing expenses in retirement, even ahead of travel or entertainment spending. That trend forces retirees to treat every COLA announcement with cautious optimism instead of celebration.

How a Smaller Net COLA Increase Affects Everyday Retirement Life

A shrinking COLA boost creates real-world problems that extend far beyond disappointing numbers on a benefits statement. Retirees who already operate on tight monthly budgets may need to delay dental work, skip vacations, reduce charitable giving, or cut back on dining out to absorb higher healthcare deductions. Rising Medicare premiums also hit hardest in areas where housing, groceries, and utilities already consume a huge share of fixed income budgets. Someone living on $1,900 per month in Social Security benefits may feel every lost dollar immediately after automatic deductions kick in. Even modest premium hikes can quickly snowball into difficult financial choices when inflation continues squeezing household expenses from every direction.

Many seniors respond by searching for cheaper insurance supplements, switching prescription plans, or hunting aggressively for discounts at grocery stores and pharmacies. Retirees with chronic health conditions face even tougher situations because they cannot simply reduce medical spending without risking their health. Financial stress also creates emotional strain that affects sleep, mental health, and overall quality of life during retirement years that should feel more stable. Some older Americans even return to part-time work because fixed income payments no longer cover basic living costs comfortably. That growing reality has transformed retirement planning into a much more complicated balancing act than previous generations experienced.

The Hidden Budget Trap Many Seniors Never See Coming

Medicare premium increases rarely arrive alone, which makes the financial impact even more frustrating for retirees. Property taxes, homeowners insurance premiums, food prices, and utility bills often rise during the same period that Medicare deductions increase. Seniors living in regions with high energy costs or expensive housing markets frequently feel trapped between essential expenses that all demand more money at once. Retirees who carry lingering credit card balances or medical debt face even greater pressure because interest charges continue piling up every month. A smaller net COLA increase can suddenly turn a manageable budget into a stressful month-to-month survival plan.

Financial counselors often encourage retirees to review spending categories every quarter instead of waiting for annual budget reviews. Small adjustments like comparing prescription drug plans, reducing unused subscriptions, or negotiating insurance rates can create extra breathing room when Medicare costs rise. Emergency savings also matter more than ever because surprise expenses like home repairs or car maintenance can quickly derail a fixed-income budget. Many experts recommend that retirees build a dedicated healthcare reserve fund specifically for future premium and medication increases. That proactive approach may not eliminate rising costs, but it can soften the financial shock when new Medicare rates take effect.

With Medicare premiums on the rise, it’s time for seniors to work on their budgets – Shutterstock

Smart Moves Retirees Can Make Before Premiums Rise Again

Retirees who prepare early often handle Medicare increases with far less financial disruption than those who react after costs climb. Reviewing Medicare Advantage plans, Medigap policies, and prescription drug coverage during open enrollment can uncover meaningful savings opportunities. Some seniors also qualify for assistance programs that help reduce premiums, prescription costs, or other medical expenses, yet many never apply because they assume they earn too much to qualify. Budget experts frequently recommend tracking every monthly expense for at least three months to identify spending leaks that quietly drain retirement income. Even trimming a handful of recurring expenses can help offset higher Medicare deductions without drastically changing daily routines.

Older Americans nearing retirement should also factor rising healthcare costs into long-term financial planning instead of focusing only on housing and lifestyle expenses. Healthcare inflation rarely slows for long, and Medicare costs will likely continue climbing as the population ages and medical treatments become more expensive. Retirees who maintain flexible budgets usually adapt more successfully when surprise premium increases arrive. Financial planners often suggest building multiple income streams through retirement savings, pensions, or part-time work to reduce reliance on Social Security alone. That strategy can provide valuable breathing room when COLA increases fail to keep pace with healthcare costs.

The Retirement Reality Check Many Americans Now Face

The upcoming Medicare premium increase highlights a harsh financial reality that millions of retirees already feel every month. Social Security COLA boosts may still provide valuable help, but higher healthcare costs continue swallowing larger portions of those increases before retirees can use the money elsewhere. Seniors who plan carefully, monitor expenses closely, and explore available assistance programs stand a better chance of protecting their financial stability. Retirement no longer guarantees predictable monthly costs, especially as healthcare spending keeps climbing faster than many fixed incomes. The growing gap between COLA increases and Medicare premiums will likely remain one of the biggest financial challenges older Americans face in the years ahead.

What changes have rising Medicare costs forced in your own retirement budget, and do you think Social Security COLA increases still keep pace with real-life expenses?

Brandon Marcus is a writer who has been sharing the written word since a very young age. His interests include sports, history, pop culture, and so much more. When he isn’t writing, he spends his time jogging, drinking coffee, or attempting to read a long book he may never complete.

Some retirement costs hit seniors hard than others, according to financial advisors – Shutterstock

Retirement looks relaxing in commercials. A couple sips coffee by the lake, someone plays golf at noon, and every financial problem magically disappears after age 65. Real life tells a very different story. Many retirees enter their golden years with solid savings and a paid-off home, yet unexpected expenses still punch giant holes through their budgets.

Financial advisors see the same painful surprises again and again. Healthcare costs rise faster than expected, adult children need financial help, and everyday living expenses keep climbing long after paychecks stop. Americans over 60 often prepare for the obvious bills while completely missing the sneaky ones that quietly drain retirement accounts month after month.

1. Healthcare Costs That Keep Growing Every Year

Healthcare expenses shock retirees because Medicare does not cover nearly as much as many people expect. Monthly premiums, prescription drugs, dental care, vision expenses, hearing aids, and copays add up fast. A healthy 65-year-old couple may spend hundreds of thousands of dollars on healthcare throughout retirement, according to estimates from Fidelity, and many retirees never fully prepare for that reality. One unexpected surgery or chronic illness can suddenly reshape an entire financial plan. Financial advisors often warn clients that healthcare inflation tends to move faster than regular inflation, which makes these costs especially dangerous over a 20- or 30-year retirement.

Long-term care creates an even bigger financial landmine. Assisted living facilities, in-home nursing care, and memory care services can cost thousands every single month. Many families assume Medicare will handle these expenses, but Medicare usually covers only limited short-term care needs. Advisors frequently see retirees burn through savings accounts far faster than expected once long-term care enters the picture. Some retirees even end up selling homes or relying heavily on family members to stay financially afloat during serious health events.

2. Helping Adult Children Financially

Many retirees expect their biggest financial responsibility to end once their children leave home. Instead, plenty of Americans over 60 continue supporting adult children well into retirement. Rising housing costs, student loan debt, childcare expenses, and job instability push many younger adults back toward their parents for financial help. Advisors regularly see retirees covering rent payments, emergency bills, car repairs, and even groceries for grown children.

These ongoing expenses often start small and quietly expand over time. A parent helps with one medical bill, then assists with a down payment, then starts babysitting several days each week to reduce daycare costs. Some retirees dip into retirement savings far earlier than planned because they want to help family members stay afloat. Financial advisors caution that generosity can create major long-term problems when retirees sacrifice their own financial security. Many retirees struggle emotionally with setting boundaries, especially when grandchildren enter the equation.

3. Home Maintenance Never Really Stops

Retirees often assume housing costs shrink dramatically once the mortgage disappears. Unfortunately, homes continue demanding money long after the final mortgage payment clears. Roof replacements, plumbing leaks, HVAC systems, property taxes, insurance increases, and appliance failures can hammer retirement budgets without warning. Advisors frequently remind clients that older homes usually become more expensive to maintain, not less expensive.

Even retirees who downsize face surprise expenses. Condo association fees can rise sharply, and retirement communities often charge additional maintenance assessments. A simple kitchen remodel or bathroom upgrade for aging-in-place safety can cost tens of thousands of dollars. Financial planners regularly encourage retirees to maintain a dedicated home repair fund because unexpected repairs rarely arrive at convenient times. Nobody wants to spend retirement arguing with a water heater that suddenly quits in the middle of January.

Seniors must be mindful of home mainteance costs – Shutterstock

4. Inflation Eats Away at Fixed Income

Inflation quietly attacks retirees in ways many people underestimate before retirement begins. Workers usually receive raises or pursue better-paying jobs during their careers, but retirees often rely on fixed income streams. Even modest inflation can seriously reduce buying power over a couple decades. Grocery bills, utility costs, gas prices, insurance premiums, and restaurant meals all continue climbing while retirement income may stay relatively flat.

Financial advisors frequently point to lifestyle inflation inside retirement itself. Many retirees spend more money during the early years of retirement because they finally have time to travel, dine out, and pursue hobbies. A retirement budget that looked comfortable at age 65 can feel painfully tight by age 75. Advisors often encourage retirees to revisit spending plans yearly instead of assuming one retirement number will work forever. Inflation may seem boring during financial planning discussions, but it becomes brutally real at the grocery checkout line.

5. Taxes Do Not Disappear After Retirement

Many Americans assume taxes shrink dramatically once retirement begins. Financial advisors regularly watch retirees get blindsided by taxable retirement account withdrawals, Social Security taxation, and capital gains taxes. Traditional 401(k) and IRA withdrawals count as taxable income, and required minimum distributions can push retirees into higher tax brackets than expected.

Taxes become even more complicated when retirees juggle multiple income streams. Pension income, investment gains, part-time work, rental properties, and Social Security benefits can combine into a surprisingly large tax bill. Some retirees discover too late that they withdrew retirement funds inefficiently for years. Advisors often stress the importance of tax planning throughout retirement rather than focusing only on investment growth. A smart withdrawal strategy can potentially save retirees thousands of dollars every year.

Retirement Reality Requires More Flexibility Than Most People Expect

Retirement rarely follows a perfectly predictable script. Life changes fast, families face unexpected challenges, and costs continue shifting year after year. Financial advisors consistently emphasize flexibility because rigid retirement plans often crack under real-world pressure. Americans over 60 who stay adaptable usually handle financial surprises far better than those who assume expenses will remain stable forever.

What retirement expense do people most underestimate, and has any surprise cost changed the way retirement looks for friends or family members? Share your thoughts in the comments.

Brandon Marcus is a writer who has been sharing the written word since a very young age. His interests include sports, history, pop culture, and so much more. When he isn’t writing, he spends his time jogging, drinking coffee, or attempting to read a long book he may never complete.

The Social Security COLA in 2027 could be rising, but your checks could still be shrinking – Shutterstock

Retirees just received a fresh dose of attention-grabbing news as the 2027 Social Security COLA forecast ticks higher once again. The adjustment signals that inflation pressures continue to shape future benefits, even years ahead of payment changes. Many households feel relief at the idea of larger checks, especially after recent stretches of elevated prices. Still, that optimism deserves a closer look because several quiet forces can chip away at the final deposit amount. A bigger COLA headline does not always translate into a bigger monthly budget.

The Social Security Administration bases COLA adjustments on inflation trends measured through the Consumer Price Index for Urban Wage Earners and Clerical Workers (CPI-W). When that index rises, projections for future COLA increases also tend to climb. However, forecasts shift frequently because inflation data changes month by month. Even a small uptick in energy, housing, or healthcare costs can push expectations higher. That volatility sets the stage for both excitement and confusion among beneficiaries.

Why the 2027 COLA Forecast Is Rising Again

The latest forecast increase reflects ongoing inflation persistence in key spending categories that matter most to retirees. Housing costs continue to apply upward pressure, especially rents and property-related expenses across many regions. Healthcare services also remain sticky, with medical inflation running hotter than general inflation in several recent reporting periods. Analysts tracking these trends adjust projections to reflect that momentum, which explains the upward shift in the 2027 COLA outlook. Even modest inflation surprises can ripple forward into multi-year benefit estimates.

Energy prices and grocery costs also play a major role in shaping expectations for future COLA changes. When fuel or food prices spike, the CPI-W reacts quickly and sends signals into long-term forecasts. Economists also factor in labor market conditions because wage growth often correlates with broader inflation patterns. Together, these variables create a dynamic picture that keeps shifting rather than locking into a stable number. That constant movement explains why retirees often see forecast changes long before actual benefit adjustments arrive.

The Hidden Costs That Can Shrink a Bigger Check

Medicare premiums represent one of the most common forces that quietly reduce Social Security gains. Part B premiums typically deduct directly from monthly benefits, and those premiums often rise alongside healthcare inflation. Even when COLA increases arrive, higher Medicare costs can absorb a significant portion of that boost. Many retirees notice their net deposit barely changes even after a strong COLA year. That disconnect often surprises people who expect a direct one-to-one increase.

Taxation also plays a major role in reducing take-home Social Security income for many households. Combined income thresholds determine whether benefits face federal taxation, and inflation-driven COLA increases can push more retirees above those limits. That shift can trigger a higher tax bill, effectively offsetting part of the benefit increase. IRMAA surcharges can also increase Medicare costs for higher-income beneficiaries, adding another layer of reduction. These hidden adjustments often matter just as much as the COLA itself.

Why a Bigger COLA Doesn’t Always Equal a Bigger Budget

A rising COLA forecast often creates optimism, but real-world spending power depends on more than headline numbers. Inflation affects different categories unevenly, and retirees often feel the pressure in essentials like housing, healthcare, and utilities. When those costs rise faster than the COLA adjustment, purchasing power still declines. That mismatch creates frustration because the benefit increase looks strong on paper but weak in practice. Financial planners often describe this gap as the “inflation lag effect.”

Timing also plays a key role in how retirees experience changes in their monthly income. COLA adjustments typically arrive once per year, while inflation shifts continuously throughout all twelve months. That delay means prices can run ahead of benefits for long stretches. Some households also face rising out-of-pocket medical expenses that COLA increases cannot fully offset. The end result often feels like a race between rising costs and delayed adjustments.

How Retirees Can Prepare for a Shifting Benefit Landscape

Budget flexibility becomes one of the most effective tools for handling unpredictable COLA outcomes. Retirees often benefit from separating essential expenses from discretionary spending to create clearer financial priorities. Even small adjustments, such as reducing subscription services or renegotiating insurance plans, can offset rising costs. Planning ahead also helps reduce stress when Medicare or tax changes reduce net income. A proactive approach often creates more stability than reacting after changes occur.

Diversified income sources also help reduce reliance on Social Security alone. Savings accounts, part-time work, or retirement investments can provide buffers when benefit increases fall short of expectations. Financial advisors often recommend reviewing withdrawal strategies annually to align with inflation trends. That approach helps smooth out the impact of rising healthcare and living costs. Preparation strengthens resilience in a system that frequently shifts with economic conditions.

Retirement budgets are key, even if the COLA goes up in 2027 – Shutterstock

The Real Story Behind the COLA Hype and What Comes Next

The 2027 COLA forecast increase highlights a simple truth: inflation continues to shape retirement income in powerful ways. Even when projections rise, net benefits depend on a mix of premiums, taxes, and real-world expenses. Retirees who focus only on headline COLA numbers often miss the bigger financial picture. The system rewards awareness and planning more than reaction and optimism alone. That balance matters more than any single forecast change.

What matters most when COLA rises but expenses rise too, and how should retirees adapt their strategy moving forward? It’s time to discuss this vital topic below in our comments.

Brandon Marcus is a writer who has been sharing the written word since a very young age. His interests include sports, history, pop culture, and so much more. When he isn’t writing, he spends his time jogging, drinking coffee, or attempting to read a long book he may never complete.

California is a great place for seniors to retire but insuanrce prices are eye-popping – Shutterstock

Retirement in California continues to feel less like a fixed chapter and more like a moving target. Seniors across the state now open insurance renewal notices and immediately notice steep jumps that disrupt carefully planned budgets. Many households that once felt stable now face sudden monthly increases that force tough financial choices. Housing expenses continue to climb at the same time, leaving less breathing room for essentials like food, transportation, and medical care. Utility companies also keep adjusting rates upward, adding even more pressure to already stretched incomes.

This combination creates a financial squeeze that does not ease up with time. Seniors who rely on Social Security or fixed pensions often struggle to match income with rapidly rising expenses. Insurance renewals, in particular, have become a major shock point because increases often arrive without much warning. Families and caregivers now step in more frequently to help cover gaps or reorganize budgets. The situation reflects a broader affordability challenge that continues reshaping retirement life in the state.

Insurance Renewal Shock Hits California Seniors Hard

Insurance renewal notices across California now deliver some of the most stressful financial moments for seniors. Homeowners and renters alike report sharp premium increases that sometimes climb by double-digit percentages within a single year. Many insurance carriers point to rising wildfire risks, higher construction costs, and inflation-driven claim expenses as key reasons behind the adjustments. Seniors on fixed incomes feel these changes immediately because they rarely have room to absorb unexpected increases. A once-manageable monthly premium now competes directly with groceries, prescriptions, and transportation costs.

Some seniors respond by reducing coverage or increasing deductibles, but those choices introduce new risks. Others shop aggressively for alternative providers, yet find fewer affordable options available in high-risk regions. Insurance brokers across California note that older homeowners often feel stuck between rising premiums and limited market availability. Budget planning becomes more complicated as renewal dates approach, especially when multiple policies increase at the same time. The result creates ongoing financial uncertainty that disrupts long-term retirement stability.

Housing Costs Continue to Drain Fixed Retirement Incomes

Housing expenses in California continue to climb, placing steady pressure on seniors who remain in long-term homes or rental units. Property taxes, maintenance costs, and rent increases often rise faster than retirement income adjustments. Many seniors who expected lower expenses after retirement now face the reality of staying in high-cost housing markets. Even homeowners without mortgages still deal with rising insurance, repairs, and utility-linked housing costs. The overall cost of keeping a roof overhead continues to grow year after year.

Downsizing sounds like a logical solution, but the housing market complicates that option. Smaller homes or senior-friendly units often carry price tags that surprise retirees expecting relief. Relocation also brings emotional and financial challenges, including moving expenses and higher rental rates in some smaller communities. Seniors who stay put frequently redirect funds from other essential categories just to maintain housing stability. This ongoing pressure makes housing one of the biggest drivers of financial strain in retirement.

Utility Bills Add Another Layer of Financial Strain

Utility costs in California continue to rise, and seniors feel the impact each month when electricity, water, and gas bills arrive. Energy providers cite infrastructure upgrades, climate-related demand, and supply costs as reasons behind higher rates. Air conditioning use during hotter months creates especially noticeable spikes in electricity bills. Seniors who spend more time at home often experience higher baseline usage compared to working-age households. That reality turns utilities into a consistent and unavoidable expense category that keeps expanding.

Some seniors attempt to reduce costs by adjusting thermostats, limiting appliance use, or installing energy-efficient upgrades. However, upfront costs for upgrades often feel out of reach for households already struggling with insurance and housing increases. Water bills also rise in many areas due to conservation pricing structures and local infrastructure investments. Even small increases across multiple utility categories combine into significant monthly budget changes. These compounding expenses leave fewer financial buffers for emergencies or unexpected medical costs.

Utility bills are hurting California seniors in the pocketbook, along with insurance renewals – Shutterstock

Why Insurance Premiums Keep Rising Across the State

Insurance companies continue adjusting premiums upward due to a combination of environmental and economic pressures. Wildfire frequency and severity across California create higher risk exposure that insurers factor into pricing models. Inflation also raises the cost of rebuilding homes, replacing vehicles, and processing claims, which directly affects premium calculations. Reinsurance costs, which insurers pay to protect themselves from large-scale losses, continue climbing as well. All these factors work together to push renewal prices higher for consumers.

Regulatory changes and regional risk assessments also influence how insurers structure coverage in different counties. High-risk zones often see fewer providers, which reduces competition and contributes to higher pricing. Seniors who live in long-established homes sometimes feel particularly affected because their properties sit in areas now classified as higher risk than in previous decades. Insurance markets respond quickly to new data, but consumers often experience the financial impact immediately. This gap between risk modeling and household affordability creates ongoing tension for retirees.

Seniors across California increasingly look for practical strategies to manage rising insurance, housing, and utility costs. Many review insurance policies annually to compare coverage levels and identify possible discounts tied to bundling or safety upgrades. Local assistance programs sometimes help offset utility bills, especially for low-income retirees who qualify for energy support. Budget restructuring also plays a key role as seniors prioritize essential expenses and reduce discretionary spending. Financial advisors often recommend building small emergency buffers even during tight income periods.

Community resources and senior advocacy organizations also provide guidance on cost-saving opportunities that many households overlook. Some retirees explore shared housing or cooperative living arrangements to reduce housing pressure without leaving familiar communities. Energy efficiency improvements, even small ones like LED lighting or improved insulation, help reduce long-term utility expenses. Careful planning around renewal dates for insurance policies helps prevent surprise budget disruptions. These combined strategies create more stability, even in an environment where costs continue to rise.

The Reality Behind California’s Retirement Cost Crunch

California seniors now navigate a financial landscape shaped by rising insurance renewals, housing pressure, and increasing utility costs. Each category alone presents challenges, but together they create a compounding effect that strains even well-planned retirement budgets. Many households now adjust spending monthly instead of yearly just to stay ahead of changes. Financial resilience depends more on flexibility and awareness than ever before. The situation continues evolving, but seniors who track costs closely and explore available support options gain more control over their financial stability.

What changes would make retirement more sustainable where cost pressures keep rising?

Brandon Marcus is a writer who has been sharing the written word since a very young age. His interests include sports, history, pop culture, and so much more. When he isn’t writing, he spends his time jogging, drinking coffee, or attempting to read a long book he may never complete.

A tight grocery budget can hurt seniors living check to check – Shutterstock

That projected $81 monthly COLA increase might sound like a helpful boost for Social Security recipients, but everyday costs can swallow it fast. Prices keep shifting across essential categories, and many seniors already juggle tight budgets. Small expenses add up quickly when they hit month after month without warning.

The reality is that even modest increases in benefits often struggle to keep pace with real-life spending pressures. Here are nine common expenses that could quietly erase that COLA gain before the month even settles in.

1. Grocery Bills That Refuse to Cool Down

Grocery stores continue to reflect stubbornly high food prices across many basic categories. Seniors often prioritize fresh produce, dairy, and protein, which have seen some of the steepest increases. Even a slight weekly uptick of $10 to $15 can consume a large chunk of that $81 boost. Store loyalty programs help, but they rarely offset inflation entirely. Many shoppers now notice fewer items in the cart for the same budget.

Food costs also fluctuate based on seasonality and supply chain pressures. Staples like eggs, meat, and coffee frequently swing in price without warning. Seniors on fixed incomes feel those changes immediately at checkout. Over a month, those increases often exceed the COLA gain entirely.

2. Prescription Drug Copays and Pharmacy Costs

Prescription medications often come with rising copays, even for insured seniors. A single medication adjustment can add $20 or more per month in out-of-pocket costs. Pharmacies also adjust pricing structures based on insurance coverage tiers. Those small differences create a noticeable dent in limited budgets.

Some seniors require multiple prescriptions, which compounds the issue quickly. Even mail-order discounts fail to fully shield against rising costs. A few medication changes can easily consume the entire COLA increase. Health needs rarely pause for financial planning.

3. Utility Bills That Keep Creeping Up

Electricity and natural gas prices fluctuate based on demand, weather, and regional supply conditions. Seniors often keep heating or cooling systems running longer due to health sensitivity. That habit drives monthly utility bills higher than expected. Even a $10 to $20 increase in energy costs wipes out a significant portion of COLA gains.

Water and sewer fees also trend upward in many municipalities. Utility companies regularly adjust base rates regardless of usage. Seniors on fixed incomes often struggle to reduce consumption further. Basic comfort now competes directly with budget limits.

4. Transportation and Fuel Expenses

Gas prices continue to shift, creating unpredictable transportation costs for seniors who still drive. Even occasional errands can add up quickly when fuel prices spike. A few extra trips per month can easily consume $30 or more. Vehicle maintenance costs also rise alongside aging cars.

Public transportation fares have increased in several regions as well. Seniors who rely on buses or rideshares feel those changes immediately. Mobility remains essential for healthcare visits and daily errands. Transportation costs rarely stay stable long enough to budget comfortably.

5. Home Maintenance and Minor Repairs

Small home repairs often arrive without warning and carry surprisingly high price tags. A leaking faucet, broken appliance, or furnace tune-up can cost $50 to $150 or more. Even minor fixes can wipe out the entire COLA increase in one visit. Homeownership continues to demand ongoing financial attention.

Older homes typically require more frequent maintenance. Aging systems tend to fail at inconvenient times. Seniors often prioritize repairs for safety reasons, regardless of cost. These unexpected expenses disrupt even the most careful budgets.

6. Insurance Premium Adjustments

Home, auto, and supplemental health insurance premiums continue to rise across many regions. Even small monthly increases reduce the value of any COLA adjustment. A $15 hike in a single policy already cuts deeply into the $81 boost. Many seniors carry multiple policies that increase simultaneously.

Insurers often adjust rates based on inflation, repair costs, and risk factors. Seniors rarely have control over those pricing decisions. Switching providers may not always reduce expenses either. Insurance remains a necessary but rising cost category.

7. Internet and Phone Service Fees

Telecom companies frequently adjust monthly service rates and equipment fees. Seniors rely heavily on phone and internet access for healthcare, communication, and banking. Even modest price hikes of $5 to $10 per service quickly stack up. Bundled packages often hide incremental increases.

Contract changes and promotional expirations also affect bills. Many seniors discover unexpected charges after introductory rates expire. Digital access remains essential for modern daily life. Connectivity costs continue to climb quietly in the background.

8. Dental and Vision Care Costs

Routine dental cleanings and vision checkups often come with out-of-pocket expenses. Medicare coverage limitations leave many seniors paying directly for these services. A single appointment can consume half or more of the COLA increase. Additional procedures drive costs even higher.

Eyeglasses, contact lenses, and dental work rarely come cheap. Providers also adjust pricing based on materials and technology. Seniors often delay care due to cost concerns. That delay can lead to larger expenses later.

Regular dental visits can get pricey for seniors living on Social Security – Shutterstock

9. Everyday Convenience Fees and Small Subscriptions

Streaming services, delivery apps, and digital subscriptions continue to multiply in many households. Even $5 to $15 monthly fees add up quickly when stacked together. Seniors often subscribe for entertainment, convenience, or essential services. These recurring charges quietly absorb extra income.

Banking fees and service charges also contribute to monthly expenses. Small automatic payments often go unnoticed until budgets tighten. Canceling subscriptions requires regular review and attention. These micro-costs collectively erase the impact of modest COLA increases.

Where That $81 Really Goes

That projected COLA increase may feel helpful on paper, but daily expenses quickly reshape its impact. Rising costs across essentials like food, healthcare, and utilities leave little breathing room. Seniors often discover that small increases vanish within routine spending cycles. Budget awareness becomes more important than ever in managing fixed income stability. Careful tracking of recurring costs can help protect financial balance even when inflation refuses to slow down.

What everyday expense do you think eats up the biggest share of a fixed income budget today?

Brandon Marcus is a writer who has been sharing the written word since a very young age. His interests include sports, history, pop culture, and so much more. When he isn’t writing, he spends his time jogging, drinking coffee, or attempting to read a long book he may never complete.

Certain Medicare costs are rising too fast to keep up with any Social Security COLA changes that will come in 2027 – Shutterstock

Retirees across America face a financial squeeze as Medicare expenses continue climbing faster than projected Social Security COLA adjustments for 2027. Many households already stretch fixed incomes, and healthcare costs keep tightening that gap in frustrating ways. Inflation in medical services, prescription pricing, and insurance overhead drives much of this pressure. Seniors who once planned comfortably now watch small increases stack up into serious monthly strain. The challenge now centers on how quickly Medicare costs outpace retirement income growth.

The 2027 COLA forecast aims to adjust Social Security benefits, but Medicare spending often moves at a faster and less predictable pace. That imbalance forces many retirees to rethink budgets, coverage choices, and even healthcare usage habits.

1. Medicare Part B Premiums Keep Climbing Steadily

Medicare Part B premiums continue rising as outpatient care costs expand across the healthcare system. Doctors, labs, and outpatient procedures all charge more as technology and staffing costs increase. Many retirees feel the impact immediately since Part B premiums deduct directly from Social Security checks. Even small monthly increases reduce take-home retirement income in a noticeable way. That steady climb often outpaces modest COLA adjustments.

Government adjustments try to balance program funding, yet demand for outpatient services keeps pushing costs upward. More seniors use preventive care and specialist visits, which adds long-term pressure to the system. Administrative expenses also contribute to higher premiums year after year. Retirees who track these changes often spot a pattern of consistent upward movement that rarely slows.

2. Medicare Part D Prescription Drug Costs Continue to Surge

Medicare Part D plans show rising costs as prescription drug pricing continues to escalate across the United States. Pharmacies pass along higher manufacturer prices, and insurers adjust premiums to match those increases. Many seniors rely heavily on medications for chronic conditions, which makes this category especially sensitive. Even small price shifts create real budget stress for fixed-income households. The pressure intensifies as more specialty drugs enter the market.

Drug manufacturers introduce new treatments at premium prices, which reshapes plan costs each year. Insurers respond by increasing deductibles and shifting more expenses onto members. Seniors often notice higher copays at the pharmacy counter before they see changes in plan documents. That gap between expectation and reality creates financial surprises that strain retirement planning.

3. Medicare Advantage Premiums and Fees Continue Their Upward Trend

Medicare Advantage plans attract millions of retirees, yet their premiums and fees continue rising faster than many expect. Private insurers adjust pricing based on regional healthcare costs and utilization patterns. Increased demand for supplemental benefits like dental and vision also drives higher plan expenses. Many seniors choose these plans for added coverage, but that choice often brings rising monthly costs. Budget flexibility becomes harder to maintain when premiums climb year after year.

Insurance companies also face higher hospital and specialist reimbursement rates, which feed directly into plan pricing. Extra perks like transportation services and wellness programs add value but increase overall cost structures. Retirees often compare plans yearly and still encounter upward pricing trends across most options. That consistency signals a broader shift in Medicare Advantage economics.

4. Prescription Drug Copays and Coinsurance Hit Harder at the Pharmacy

Out-of-pocket prescription drug costs continue rising even for insured Medicare members. Copays and coinsurance amounts increase when drug tiers shift or plan formularies change. Seniors managing multiple medications feel these changes most intensely at the pharmacy counter. Each refill adds up, especially for chronic conditions requiring long-term treatment. Budget planning becomes more difficult when costs fluctuate monthly.

Pharmacies adjust pricing structures based on insurer contracts and drug availability. Specialty medications often carry higher coinsurance percentages, which adds pressure quickly. Even generic drugs sometimes see price adjustments when supply chains tighten. That unpredictability creates frustration for retirees trying to maintain stable monthly expenses.

Prescription costs seem to be skyrocketing, which the 2027 COLA adjustments may not cover – Shutterstock

5. Medicare Part A Hospital Costs Create Bigger Financial Gaps

Hospital stays under Medicare Part A still involve deductibles and coinsurance that continue rising over time. A single hospital admission can generate significant out-of-pocket costs even with coverage. Longer stays increase financial exposure as daily coinsurance adds up quickly. Many retirees underestimate these expenses until they face a medical emergency. That gap between expectation and reality creates real financial shock.

Hospitals across the country face higher staffing and supply costs, which pushes overall service pricing upward. Medicare adjusts coverage thresholds, but beneficiaries still absorb a portion of those increases. Emergency care and inpatient services remain among the most expensive healthcare experiences. Planning for these costs becomes essential for anyone relying on Medicare coverage.

6. Medigap Premiums Increase as Private Insurance Costs Rise

Medigap plans help cover Medicare gaps, yet premiums continue rising due to private insurance market pressures. Insurers adjust pricing based on age, claims history, and regional healthcare inflation. Many retirees rely on these plans to reduce unexpected out-of-pocket expenses. Higher premiums reduce the savings advantage these plans once offered. That shift forces many seniors to reassess coverage annually.

Healthcare providers charge more for services, and Medigap insurers pass those costs through to members. Administrative costs and claim volumes also influence yearly premium adjustments. Seniors who keep these plans often notice steady increases that outpace general inflation. That trend makes long-term planning more challenging for fixed incomes.

7. Skilled Nursing and Long-Term Care Exposure Adds Major Risk

Skilled nursing facility costs continue rising as demand for post-hospital care increases nationwide. Medicare covers limited stays, yet coinsurance kicks in quickly after short coverage windows. Many families face unexpected expenses when recovery requires extended care. That financial burden often exceeds what retirees planned for in retirement savings. The gap between coverage and real-world needs creates major stress.

Long-term care demand grows as the population ages and chronic conditions increase. Facilities raise prices due to staffing shortages and higher operational costs. Medicare provides only partial relief, which leaves families responsible for significant portions of bills. Planning ahead becomes critical as this category carries some of the highest financial risk.

What Rising Medicare Costs Mean for Retirement Security Ahead of 2027

Medicare costs continue rising across nearly every major category, and those increases consistently outpace the projected 2027 Social Security COLA. Retirees feel the strain most when multiple cost categories rise at the same time. Budget planning grows more complex as premiums, copays, and deductibles all move upward together. Many households now focus on coverage reviews, cost comparisons, and supplemental protections to reduce exposure. The gap between healthcare inflation and retirement income growth demands closer attention than ever before.

What strategies have helped manage rising healthcare costs in your retirement, and how have those changes affected monthly budgets?

Brandon Marcus is a writer who has been sharing the written word since a very young age. His interests include sports, history, pop culture, and so much more. When he isn’t writing, he spends his time jogging, drinking coffee, or attempting to read a long book he may never complete.

Texas seniors are having to cut back on important spending due to property insurance premiums – Shutterstock

Texas property insurance costs jumped sharply last year, shaking up retirement budgets across the state. Some counties reported premium increases topping 20%, creating immediate strain for homeowners on fixed incomes. Rising storm risks, higher reconstruction costs, and surging reinsurance prices all pushed insurers to raise rates. Many retirees who planned carefully for retirement now face unexpected financial pressure that disrupts monthly stability. A typical homeowner in hard-hit areas now pays hundreds more per year just to maintain basic coverage.

Retirees across coastal and storm-prone regions feel the pressure the most, especially those living on Social Security and modest pensions. Insurance bills now compete directly with essentials like groceries, utilities, and medication. Some seniors report opening renewal letters with shock after years of steady or predictable rates. A retiree in South Texas, for example, may now pay significantly more than just two years ago for the same coverage level. Financial planners warn that this trend could reshape retirement security in high-risk states like Texas.

The Everyday Cuts Retirees Are Making to Stay Afloat

Rising insurance premiums force many Texas retirees to make immediate lifestyle adjustments. Grocery budgets shrink as seniors swap fresh produce and protein-heavy items for cheaper pantry staples. Utility usage drops as households carefully track air conditioning and heating to control monthly bills. Some retirees pause home maintenance projects, delaying roof repairs or landscaping work to preserve cash flow. Even small expenses like streaming services or community club memberships disappear from monthly budgets.

Transportation habits also shift as retirees reduce driving to save on gas and vehicle maintenance. Many seniors now cluster errands into single trips instead of multiple weekly outings. Dining out becomes rare, reserved only for special occasions rather than routine social activity. Emergency savings accounts shrink as insurance premiums consume a larger share of fixed income. These daily trade-offs reveal how sharply housing-related costs ripple through every part of retirement life.

Why Texas Premiums Keep Climbing Faster Than Inflation

Insurance companies in Texas face mounting pressure from repeated severe weather events, including hurricanes, hailstorms, and flooding. These disasters increase claim payouts and push insurers to rebuild financial reserves more aggressively. Reinsurance costs, which insurers pay to protect themselves, also rise quickly as global disaster risks grow. Construction costs in Texas continue to climb, making home repairs and rebuilding significantly more expensive after storms. These combined pressures force insurers to adjust premiums faster than general inflation rates.

Population growth in high-risk regions adds another layer of complexity to pricing models. More homes in storm-prone zones increase the total exposure insurers must cover. Fraud prevention costs and legal expenses also rise, contributing to higher overall operational costs. Regulators attempt to balance affordability with insurer stability, but market realities often dominate pricing decisions. Texas homeowners now experience a market where risk and cost increasingly shape every renewal notice.

Smart Ways Seniors Are Fighting Back Against Rising Costs

Some Texas retirees actively shop around for new insurance providers to find better rates. Comparison shopping often reveals significant differences between carriers for nearly identical coverage. Bundling home and auto insurance policies sometimes unlocks meaningful discounts for fixed-income households. Higher deductibles also lower monthly premiums, though this strategy requires careful risk planning. Seniors increasingly consult independent insurance brokers to navigate complex policy options.

Home upgrades also play a major role in lowering premiums over time. Impact-resistant roofs, storm shutters, and updated plumbing systems can reduce risk profiles in the eyes of insurers. Some counties even offer mitigation grants that help retirees fund these improvements. Community groups and senior organizations provide education sessions on cost-saving insurance strategies. These proactive steps help retirees regain some control over rising housing expenses.

Texas is a beautiful place to live, but rising home insurance premiums are costing seniors – Shutterstock

What This Means for Texas Retirement Security Moving Forward

Texas retirement security now faces a growing challenge as housing costs consume a larger share of fixed incomes. Insurance premiums alone now rival property tax increases in their impact on monthly budgets. Seniors who planned retirement around stable housing expenses now rethink long-term financial strategies. Some retirees consider downsizing or relocating to lower-risk areas to stabilize costs. Financial advisors emphasize that housing affordability now sits at the center of retirement planning discussions.

How should retirees balance rising home protection costs with the need to preserve financial stability in retirement? We want your advice, experiences, and stories shared below in our comments section.

Brandon Marcus is a writer who has been sharing the written word since a very young age. His interests include sports, history, pop culture, and so much more. When he isn’t writing, he spends his time jogging, drinking coffee, or attempting to read a long book he may never complete.

A Social Security check from the SSA – Shutterstock

For millions of retirees, Social Security day is a little like payday with fewer surprises and a lot more budgeting. That’s why recent reports of smaller monthly checks sparked instant panic across kitchen tables and retirement communities nationwide. Many seniors assumed Washington quietly slashed benefits behind the scenes, but the reality looks far more complicated—and far more frustrating. In many cases, retirees still qualify for the same benefit amount on paper, yet the actual deposit hitting bank accounts shrank for completely different reasons. That distinction matters because the problem often comes from rising deductions, income-related costs, or repayment adjustments instead of an official cut from the Social Security Administration.

The confusion makes perfect sense because retirees usually focus on the number that lands in checking accounts each month. When that number drops, people naturally assume benefits fell across the board. However, several financial factors now chip away at monthly payments before the money even arrives. Medicare premiums jumped for some recipients, tax withholding increased for others, and overpayment recovery rules restarted after a pandemic-era pause. Those changes created a painful surprise for retirees already stretching every dollar to cover groceries, utilities, prescriptions, and housing costs.

Medicare Premiums Continue To Eat Into Monthly Checks

Medicare Part B premiums remain one of the biggest reasons retirees suddenly see smaller Social Security deposits. Most beneficiaries have those premiums deducted automatically before the payment reaches their bank accounts, which means even modest increases can feel painful on a fixed income. In 2026, higher-income retirees will also continue facing Income-Related Monthly Adjustment Amount charges, commonly called IRMAA surcharges, which can dramatically increase healthcare costs. A retiree who crossed an income threshold because of a one-time retirement account withdrawal or home sale may suddenly pay hundreds more each month. That extra deduction often catches people off guard because the surcharge gets calculated using tax returns from two years earlier rather than current income.

Healthcare inflation continues to squeeze retirees from every direction, and Medicare deductions hit especially hard because they happen automatically. Many retirees expected their annual cost-of-living adjustment to provide breathing room, only to watch Medicare premiums swallow much of the increase before they ever saw the money. Someone receiving a modest Social Security bump may still feel poorer if prescription costs, supplemental insurance premiums, and medical copays rise simultaneously. Financial planners frequently warn retirees about this exact scenario because healthcare spending tends to rise faster with age. Unfortunately, many seniors discover the impact only after opening a smaller-than-expected deposit notification from their bank.

Social Security Overpayment Collections Returned With Force

Another major reason for shrinking checks comes from the government restarting aggressive overpayment recovery efforts. During the pandemic, the Social Security Administration temporarily paused some collection activities, giving many retirees breathing room during an economically uncertain period. That pause ended, and beneficiaries who received accidental overpayments years ago now face deductions from their monthly benefits. In some cases, retirees had no idea they received too much money until the government mailed a notice demanding repayment. The resulting reductions stunned seniors who already built their monthly budgets around every dollar of their expected income.

Overpayments happen more often than many Americans realize, especially when retirees continue working while collecting benefits or fail to report life changes quickly. The Social Security Administration may later determine that a recipient earned too much income, experienced a marital-status change, or qualified for a different payment amount than originally calculated. Once the agency identifies the issue, it can withhold part of future benefits until the balance gets repaid. Some retirees lose only a small portion of their checks each month, while others face far steeper reductions depending on the amount owed. Advocacy groups continue pressuring lawmakers to reform the process because many seniors say the repayment demands create severe financial hardship.

Taxes Surprise Retirees More Than Expected

Many Americans enter retirement assuming Social Security benefits arrive tax-free, but reality tells a different story for millions of households. Federal taxes can apply to Social Security income when retirees exceed certain income thresholds, and some states also tax benefits. Retirees who continue part-time work, withdraw larger amounts from retirement accounts, or receive investment income may suddenly owe more taxes than expected. Some recipients voluntarily choose withholding from their monthly checks to avoid a large tax bill later, which directly lowers the amount deposited each month. Others discover their benefits shrank after the IRS adjusted withholding requirements based on income changes.

Inflation and higher interest rates created another sneaky problem for retirees who rely on savings accounts or certificates of deposit. Those higher yields boosted taxable income for many seniors, which sometimes pushed them into higher taxation ranges for Social Security benefits. A retiree who suddenly earned stronger interest income may celebrate better returns while simultaneously watching Social Security withholding rise. Financial advisors increasingly encourage retirees to coordinate withdrawals carefully across taxable accounts, Roth accounts, and traditional retirement plans to avoid unnecessary tax hits. Without a clear strategy, retirees can accidentally trigger larger deductions that quietly reduce their monthly checks.

COLA Increases Don’t Always Feel Like Raises

Every year, headlines celebrate Social Security cost-of-living adjustments as financial relief for seniors battling inflation. Unfortunately, many retirees never fully experience those increases because rising costs erase the gains almost immediately. A 2% or 3% COLA sounds helpful until Medicare premiums, housing costs, groceries, and utility bills climb even faster. Retirees often compare current deposits to previous years and wonder why their “raise” somehow left them with less spending power. That disconnect fuels frustration because the official benefit technically increased even while real-life affordability declined.

Fixed-income households feel inflation differently than younger working Americans because retirees spend larger portions of their budgets on essentials. Food, healthcare, insurance, and housing dominate retirement spending, and those categories experienced sharp price increases over the past several years. A retiree may receive an additional $50 per month from a COLA adjustment while simultaneously paying $80 more for Medicare, medications, and household bills. Economists regularly debate whether the government’s inflation formula accurately reflects senior spending patterns. Until that debate changes policy, many retirees will continue feeling financially squeezed despite receiving larger official benefit amounts.

A senior man, frustrated by the size of his Social Security check – Unsplash

The Retirement Reality Many Americans Didn’t Expect

Retirement once carried images of financial stability, afternoon golf games, and stress-free living after decades of hard work. Today’s retirees face a very different environment filled with rising healthcare costs, stubborn inflation, and complex benefit rules that can reduce monthly income without warning. Smaller Social Security checks now reflect a broader financial reality rather than a simple government benefit cut. Americans approaching retirement increasingly need detailed planning strategies that account for taxes, Medicare premiums, and unexpected repayment issues before those expenses derail monthly budgets. Staying proactive, reviewing benefit statements carefully, and consulting qualified financial professionals can help retirees avoid unpleasant surprises later.

What changes have affected your retirement finances the most in recent years, and do current Social Security adjustments feel fair? Our comments section is the perfect place to talk about this topic.

Brandon Marcus is a writer who has been sharing the written word since a very young age. His interests include sports, history, pop culture, and so much more. When he isn’t writing, he spends his time jogging, drinking coffee, or attempting to read a long book he may never complete.

A couple of retirees going over their finances – Shutterstock

Retirement planning has never felt more like a moving target than it does right now. New tax rules continue to shift how much retirees keep versus how much goes back to the IRS, and those changes can quietly reshape long-term financial security. Many savers focus on building their nest egg but overlook how withdrawals, conversions, and income timing interact with updated tax brackets.

Small missteps can snowball into thousands of dollars lost over a retirement that might last decades. Smart planning now matters more than ever because the rules keep tightening around traditional strategies.

1. Missing the Timing Window for Roth Conversions

Roth conversions look simple on paper, but timing under new tax rules can make or break their value. Many retirees push conversions too late, landing themselves in higher tax brackets when required minimum distributions kick in. That delay often turns a strategic move into a costly one. The IRS tax structure now rewards earlier, well-planned conversions during lower-income years. Acting without a clear timeline creates unnecessary tax spikes that erode long-term savings.

Retirees who stagger conversions over several years often preserve more wealth than those who rush the process. Strategic planning helps smooth out taxable income instead of stacking it into one painful year. New rules around income thresholds make this even more important for middle- and upper-income households. Ignoring the timing element can quietly drain tens of thousands over time. A proactive conversion strategy helps keep retirement income far more predictable.

2. Overlooking Changes to Required Minimum Distributions

Required minimum distributions now follow stricter timelines, and many retirees still underestimate their impact. The age shift for RMDs sounds small, but it reshapes how long retirement accounts can grow tax-deferred. Missing these changes can lead to penalties that hit fast and hard. More importantly, larger forced withdrawals can push retirees into higher tax brackets without warning. That extra income can also affect Medicare premiums and other benefits.

Planning ahead for RMDs helps retirees avoid unpleasant tax surprises later in life. Coordinating withdrawals with other income sources keeps tax exposure more manageable. Many financial plans still treat RMDs as a future problem instead of a present strategy issue. That approach creates unnecessary financial pressure once distributions begin. Staying ahead of the schedule keeps retirement income smoother and more efficient.

3. Ignoring Tax Diversification Across Accounts

Too many retirement portfolios rely heavily on tax-deferred accounts without balancing taxable and Roth options. That imbalance creates a tax problem when withdrawals begin under current rules. New tax brackets punish large concentrated withdrawals more than diversified income streams. Without tax diversification, retirees lose flexibility when managing yearly income needs. That lack of control often leads to higher lifetime taxes.

Smart retirees spread assets across multiple account types to manage future tax exposure. This approach allows more control over which funds to tap in different tax environments. A diversified tax strategy also helps adjust to unexpected policy changes. Many investors underestimate how valuable flexibility becomes during retirement. Without it, tax rules dictate income instead of strategy guiding it.

4. Misjudging Social Security Tax Thresholds

Social Security benefits no longer remain fully protected from taxation once income crosses specific thresholds. Many retirees underestimate how easily required distributions and investment income push them over those limits. Once that happens, up to 85 percent of benefits may become taxable. New tax rules tighten the interaction between retirement income sources even further. That combination surprises many households that assumed their benefits stayed largely untouched.

Careful income planning helps reduce unnecessary Social Security taxation. Coordinating withdrawals from different accounts can keep taxable income under key thresholds. Even small adjustments in timing can reduce the percentage of benefits taxed. Many retirees miss this opportunity because they treat Social Security separately from other income. Viewing it as part of a larger tax picture leads to better long-term outcomes.

Beneficiary designations often receive less attention than they deserve, even though they carry major tax consequences. Outdated or poorly structured beneficiaries can trigger unexpected tax burdens for heirs. New tax rules around inherited retirement accounts make this even more critical. Mistakes here often bypass probate but still create significant tax exposure. That combination leads to financial stress for families during already difficult times.

Regularly reviewing beneficiary designations prevents unnecessary complications. Aligning accounts with current tax laws helps preserve more wealth for heirs. Many retirees forget that beneficiary rules now require faster distributions in certain cases. That acceleration can increase taxable income for beneficiaries. Careful updates ensure assets transfer more efficiently and with fewer surprises.

A retiree looking at paperwork next to his beneficiary – Shutterstock

6. Overdrawing Accounts Without Considering Capital Gains Impact

Retirees often focus on IRA withdrawals but overlook taxable brokerage accounts and capital gains implications. New tax brackets can significantly increase the cost of poorly timed asset sales. Selling investments without a strategy often triggers avoidable capital gains taxes. That mistake becomes more expensive when combined with other retirement income sources. Poor sequencing of withdrawals can reduce overall portfolio longevity.

Strategic withdrawal planning helps reduce unnecessary tax exposure from investment sales. Coordinating gains with lower-income years can soften tax impact significantly. Many retirees fail to adjust withdrawal order when tax laws shift. That oversight quietly increases lifetime tax liability. A thoughtful withdrawal sequence protects more capital for long-term needs.

A Smarter Way to Navigate Retirement Tax Rules Ahead

Retirement success depends less on how much gets saved and more on how efficiently that money gets used under evolving tax laws. Each mistake above connects directly to missed opportunities for tax savings and income optimization. The newest tax rules reward flexibility, timing, and awareness rather than rigid withdrawal habits. Retirees who adapt quickly often preserve significantly more wealth over time. Small adjustments today can prevent major financial setbacks later.

What retirement tax strategy feels most confusing right now, and what changes would make it easier to manage?

Brandon Marcus is a writer who has been sharing the written word since a very young age. His interests include sports, history, pop culture, and so much more. When he isn’t writing, he spends his time jogging, drinking coffee, or attempting to read a long book he may never complete.