At 10:20 PM ET on Wednesday night, Verizon finally plugged the leaks on a massive 10-hour software-driven blackout that left over 2 million Americans in “SOS mode.” Yesterday, the company issued an official apology and a promise: a $20.00 account credit for everyone affected.

But today, January 16, that promise of “free money” has turned into a digital landmine. Scammers have launched a massive, nationwide “smishing” (SMS phishing) campaign that is perfectly timed to exploit your wait for that $20 refund. If you click the wrong link today, you aren’t just losing your credit—you are handing over the keys to your entire financial life.

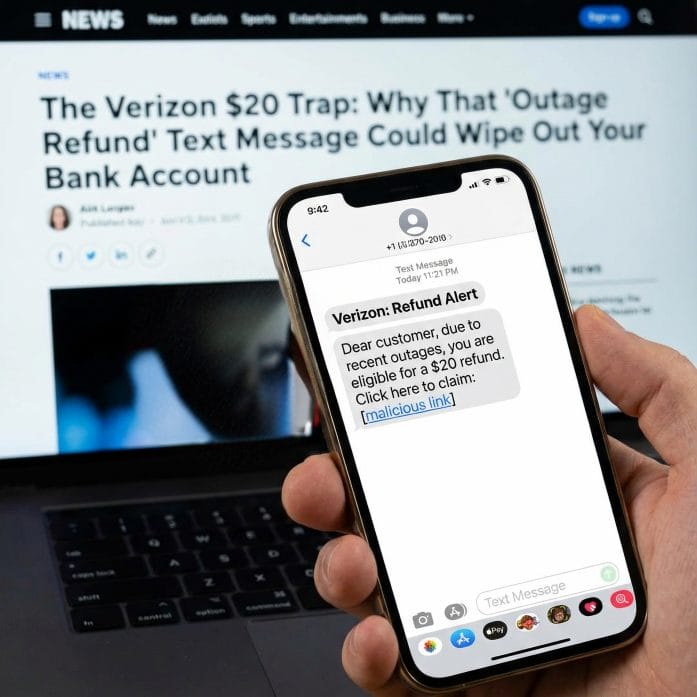

The ‘Perfect’ Scam: How They Are Hooking You

The danger lies in how Verizon decided to handle the rollout. In an official statement, Verizon News confirmed: “You will receive a text message when the credit is available.”

Hackers were waiting for exactly that sentence. This morning, thousands of Verizon customers reported receiving texts that look nearly identical to official carrier communications. They use the same corporate branding, professional tone, and—most importantly—they reference the “January 14 Outage” specifically.

The Trap: The text contains a link (e.g., https://www.google.com/search?q=vzw-relief-portal.com or verizon-claims-2026.net). When you click, you are taken to a mirror-image of the Verizon login page. Once you enter your username and password to “claim your $20,” the scammer has everything they need to bypass your security.

From a $20 Credit to a $0 Bank Balance

This isn’t just about stealing your Verizon login. Security experts are warning that this outage has become the ultimate catalyst for “SIM Swapping”—the most dangerous form of identity theft in 2026.

Once a scammer has your account credentials, they don’t just look at your bill. They initiate a SIM Swap. They convince an automated system or a customer service bot that you have a new device. Within seconds:

Your Phone Goes Dead: You lose service immediately (thinking it’s just another outage).

They Intercept Your Texts: Every 2-factor authentication (2FA) code from your bank, your 401(k) provider, and your Venmo now goes to the scammer’s phone.

The Drain: They reset your bank passwords using the “Forgot Password” feature via SMS and drain your accounts before you even realize you’ve been hacked. In a world where your phone number is your identity, losing control of your SIM means losing control of your money.

The 3 Red Flags of a Verizon Scam Text

Verizon has stated they will notify you via text, but they will NEVER ask you to click a link to provide personal or financial data. Look for these “Audit Alarms”:

The Link: If the URL isn’t verizon.com or doesn’t direct you to open the app manually, it is 100% fake.

The Urgency: Scammers use phrases like “Claim within 2 hours or the offer expires.” Verizon’s actual credit is available for at least one full billing cycle.

The Information Request: If a site asks for your Social Security Number or a Credit Card to “verify your identity” for a credit, close the tab immediately.

How to Safely Claim Your $20 Today

If you want to ensure your $20 goes into your pocket and stay out of the hands of hackers, follow the “Manual Only” rule:

Ignore the Text: Treat every incoming text as a scam, even if it looks real.

Use the App: Open the MyVerizon App directly from your phone’s home screen.

Check ‘Verizon Up’: Navigate to the “Rewards” or “Verizon Up” section. If you are eligible, the $20 credit will appear as a “Redeem” button inside the secure app environment.

The Live Agent Hack: If you don’t see it, use the app’s chat and type “Live Agent” followed by “Request credit for Jan 14 outage.”

Small Win-Big Headache

Verizon’s $20 credit covers roughly 2–3 days of service, which is a small win for a big headache. But that small win isn’t worth a compromised bank account. We are seeing reports of “SIM Swapping” spikes in New York, Dallas, and Atlanta this morning—the exact cities hit hardest by the original outage.

Have you received a suspicious text message claiming to be from Verizon today? Tell us the phone number it came from and your city in the comments below so we can alert other readers in your area.

Read More:

The Verizon Kill Switch: Why Your Phone is Still in “SOS Mode” This Morning Despite the “Fix”

14 Outrageous Laws Still Legal in America — And Nobody’s Stopped Them

Tamila McDonald is a U.S. Army veteran with 20 years of service, including five years as a military financial advisor. After retiring from the Army, she spent eight years as an AFCPE-certified personal financial advisor for wounded warriors and their families. Now she writes about personal finance and benefits programs for numerous financial websites.