Refinancing your mortgage can be a savvy financial move, but knowing when to pull the trigger is key. It’s not just about snagging a lower interest rate, it’s about improving your financial health in a meaningful way. From changing personal circumstances to shifts in the market, various signals suggest when it might be time to consider refinancing. This guide will walk you through 15 tell-tale signs that it’s time to give your mortgage a makeover.

1. Interest Rates Have Dropped

If the interest rates have gone down since you secured your original mortgage, refinancing could be a smart choice. A lower interest rate can significantly reduce your monthly payment and the total interest you pay over the life of the loan. Even a slight rate drop can make a big difference in long-term savings. It’s like getting a pay raise without having to switch jobs or ask your boss. Financial experts often suggest that a 1% rate drop should trigger a mortgage review.

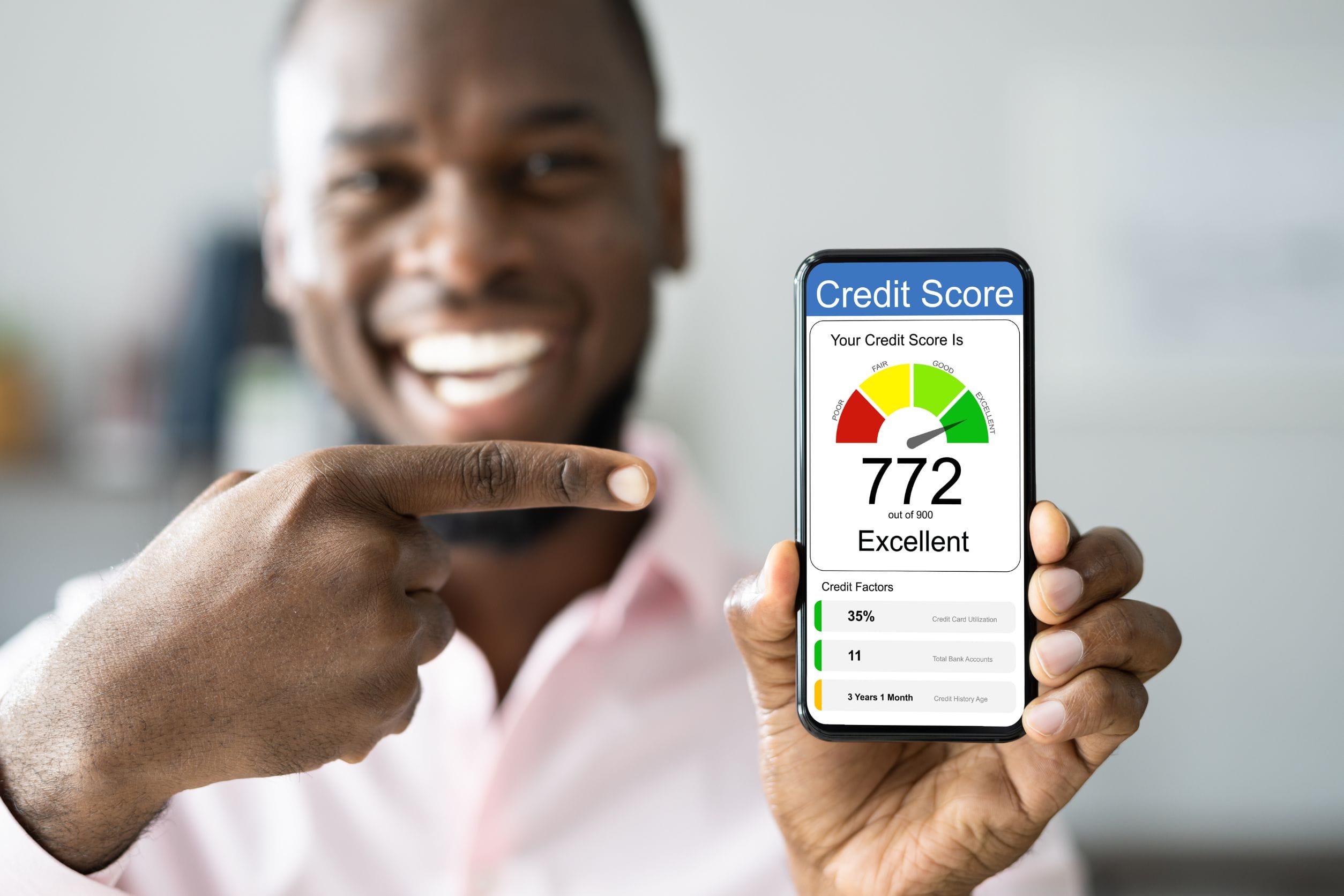

2. Your Credit Score Has Improved

An improved credit score is like a financial level-up, it gives you access to better lending terms. If your credit score has gone up since you first took out your mortgage, refinancing could secure you a lower interest rate and better loan terms. Higher credit scores signal to lenders that you’re a low-risk borrower, which could translate into substantial savings. It’s like turning a good credit history into cash savings on your home loan. So, check your credit score and see if it’s time for a mortgage tune-up.

3. You Want a Shorter Loan Term

Switching from a 30-year to a 15-year mortgage can save you a heap of money in interest over the long haul. Yes, your monthly payments will be higher, but the faster payoff means you’ll own your home outright sooner. It’s perfect for those who are eyeing retirement and want to reduce their financial burdens by then. If you can manage the bigger monthly bites, the total savings can be jaw-dropping. This move isn’t for everyone, but if you can swing it, the financial benefits are substantial.

4. You Need to Tap Into Home Equity

If your home has increased in value, you might want to tap into the equity with a cash-out refinance. This option allows you to refinance for more than you owe and pocket the difference. It’s a viable solution for funding major expenses like home renovations, college tuition, or consolidating high-interest debt. Keep in mind, though, that you’re borrowing more money, which means you’ll be paying it off longer. But if the numbers make sense, it could be a strategic financial move to free up cash when you need it most.

5. You’re Dealing with a Balloon Payment

If your current mortgage includes a balloon payment that’s due soon and you’re not ready to pay it off, refinancing can spread those costs over a new loan term. This eliminates the financial stress of coming up with a large sum all at once. Refinancing to a more traditional loan structure can provide peace of mind and budget stability. It’s a practical move for those who want to avoid the pressure of a looming large payment. For many, it’s a financial lifesaver, allowing more breathing room in their finances.

6. You Have an Adjustable-Rate Mortgage (ARM)

When you first took out your ARM, the lower initial rates were appealing. But if the adjustment period is ending and rates are on the rise, your monthly payments could start to climb, too. Refinancing to a fixed-rate mortgage locks in a rate for the remainder of your loan, providing predictable monthly expenses. It’s a great strategy for those who value budget stability over gambling with rate fluctuations. If the thought of rising payments makes you nervous, it’s time to consider switching to a fixed rate.

7. Your Financial Goals Have Shifted

Maybe you initially got a mortgage with features that no longer fit your life. Perhaps you’re making more money and can afford higher payments to shorten your loan term, or maybe you want to lower your payments to save for other investments. If your financial landscape or goals have evolved, your mortgage should evolve, too. Refinancing can adjust your financial commitments to better align with your current and future ambitions. It’s all about making your mortgage work for you, not against you.

8. There’s a Break-even Point in Sight

Refinancing usually comes with upfront costs, but it’s worth it if you can reach a break-even point relatively quickly. This is the point at which the savings from your new mortgage offset the costs of refinancing. Calculate this timing carefully, if the numbers say you’ll save more over time than you’ll spend upfront, refinancing could be a financially sound decision. It’s like investing in your financial future: a bit of cost now for savings down the road. Make sure the math works in your favor before you proceed.

9. You Want More Predictable Costs

If you’re tired of the uncertainty that comes with variable costs, refinancing a fixed-rate mortgage can smooth out your financial planning. Knowing exactly what your mortgage payment will be each month makes budgeting easier and reduces financial stress. It’s ideal for those who prefer stability in their financial life, especially if you’re planning for long-term goals like retirement. A fixed mortgage rate is like locking in your monthly expenses, giving you control over your budget. If predictability is a priority, it’s a good time to refinance.

10. Market Conditions Favor Refinancing

Sometimes, the financial market shifts in ways that make refinancing advantageous. Lower national mortgage rates, increased home values, or changes in financial regulations can all create perfect conditions for refinancing. Keeping an eye on market trends can help you decide when to make your move. It’s like catching a wave, timing is everything, and right now might be the perfect moment to catch that big financial swell. If the economic environment looks favorable, leveraging it could mean significant savings for you.

11. Major Life Changes

Significant life events like marriage, divorce, or retirement might necessitate changes in your mortgage setup. These changes can alter your financial picture dramatically, making your current mortgage less suitable. Refinancing can help you adjust your home financing to better suit your new circumstances. It’s about adapting your finances to life’s twists and turns, ensuring your mortgage doesn’t hold you back. If life has thrown you a curveball, consider whether your mortgage still fits your needs.

12. You’re Eyeing Debt Consolidation

If you’re juggling multiple high-interest debts, consolidating them into your mortgage through refinancing can simplify your finances and reduce your interest rates. This move can consolidate your debt payments into one lower-interest-rate bill, making your debts easier to manage. It’s not just about ease, though; it’s about cost-effectiveness. By folding high-interest debts into a mortgage, you could save on interest and clear your debts faster. If debt is dragging you down, refinancing might just be the lifeline you need.

13. Tax Considerations

Sometimes, refinancing can offer tax advantages that align better with your financial planning. For instance, if the tax laws have changed or if you’re looking for ways to maximize deductions, adjusting your mortgage through refinancing might make sense. It’s important to consult with a tax advisor to see how refinancing could affect your tax situation. This is about strategizing financially, not just for today but for your annual tax returns as well. If you think there’s a tax break to be had, it might be time to look into refinancing.

14. Interest-Only Period is Ending

If you’re nearing the end of the interest-only period on your mortgage, your payments are about to jump as you start paying down the principal. Refinancing can help manage this increase more smoothly by restructuring your loan. This is particularly useful if you’re not prepared for the higher monthly outlay. It’s about preventing financial strain before it happens. If a steep increase in payments is on the horizon, refinancing could offer a more manageable pathway.

15. Financial Advisers Recommend It

If your financial adviser suggests that refinancing could benefit your financial health, it’s worth taking a serious look. These professionals can provide a detailed analysis of your financial situation and the potential benefits of refinancing. Their expertise can guide you through the complexities of mortgage refinancing, ensuring that it fits your personal financial strategy. It’s like having a financial detective working out the best route for your economic journey. When in doubt, trust the experts and consider their advice seriously.

Is It Time to Refinance?

Deciding to refinance your mortgage is no small feat, but recognizing the signs can lead to substantial benefits. Whether it’s to lower payments, reduce the term, or tap into home equity, the right reasons for refinancing can bolster your financial stability and future. Each sign on this list is a potential green light to explore refinancing options, so consider your circumstances and consult with professionals. It’s all about making informed decisions that pave the way for a healthier financial life.

Read More

What Is A Guaranteed Mortgage Rate?

Mortgage life insurance for homeowners