Navigating the world of credit can be daunting, but improving your Care Credit approval odds doesn’t have to be. With the right strategies and a bit of knowledge, you can enhance your chances of getting approved. This article will guide you through essential tips and tricks to boost your Care Credit approval odds effectively.

1. Understanding Care Credit

Care Credit is a specialized credit card for healthcare expenses. It covers a range of medical services, from dental care to veterinary expenses. Knowing how it works is the first step in improving your care credit approval odds. This card offers promotional financing options, making it a popular choice for managing healthcare costs. Understanding its benefits and limitations can help you make an informed decision.

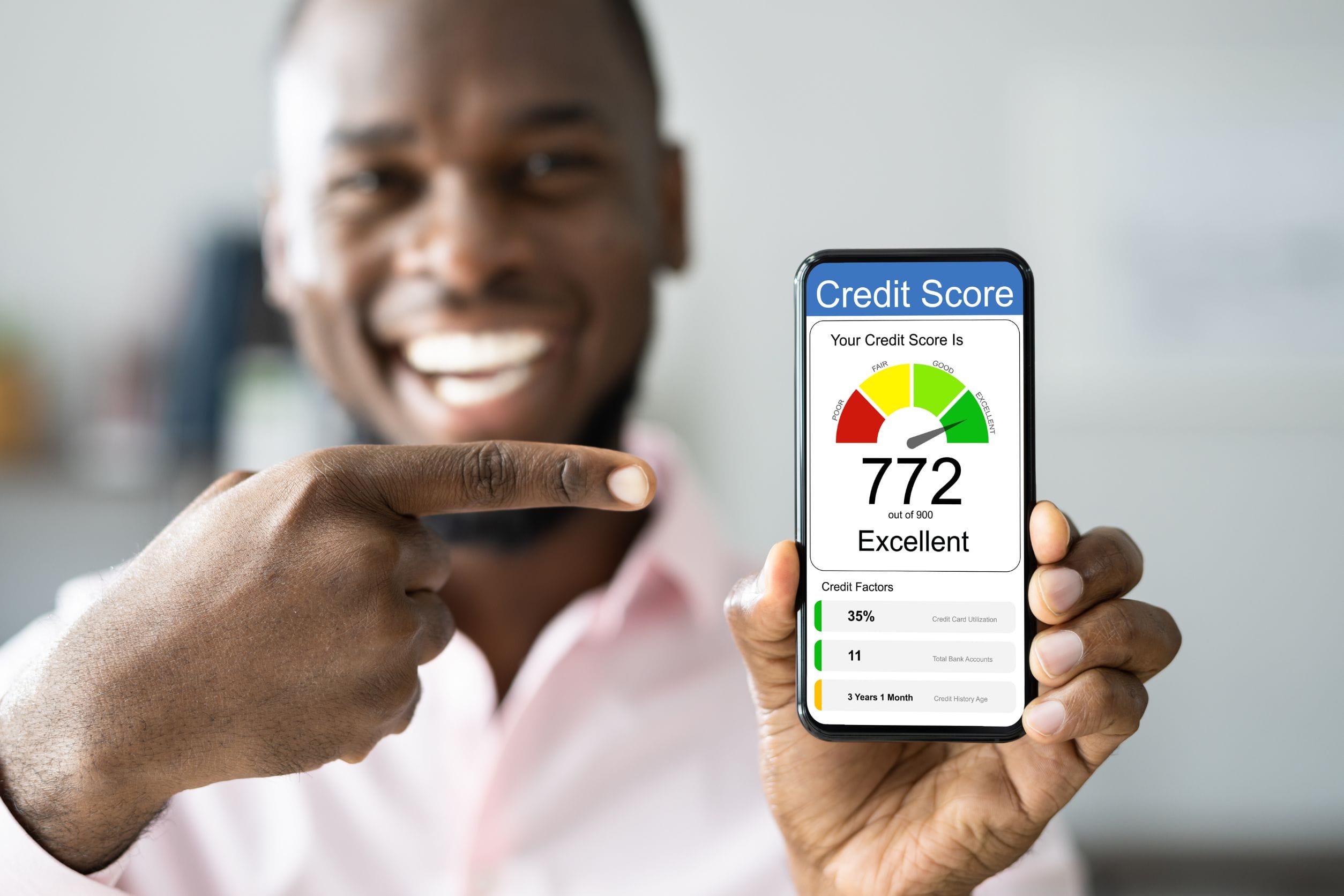

2. Check Your Credit Score

Your credit score plays a significant role in your Care Credit approval odds. Start by checking your current credit score from a reliable credit bureau. A higher score increases your chances of approval and may offer better terms. If your score is low, take steps to improve it before applying. Regularly monitoring your credit helps you stay on top of your financial health.

3. Pay Down Existing Debt

Reducing your existing debt can significantly improve your Care Credit approval odds. High levels of debt can negatively impact your credit score and your perceived ability to manage new credit. Focus on paying off credit card balances and other loans. Creating a budget to manage and reduce debt is a smart strategy. Lower debt levels signal responsible financial behavior to lenders.

4. Avoid Applying for Multiple Credit Accounts

Multiple credit applications within a short period can hurt your credit score. Each application results in a hard inquiry, which can lower your score and raise red flags for lenders. Instead, space out your credit applications and focus on improving your overall financial profile. By minimizing new credit requests, you present yourself as a less risky borrower. Patience is key in the credit approval process.

5. Ensure Your Credit Report is Accurate

Errors on your credit report can negatively affect your Care Credit approval odds. Regularly review your credit report for any inaccuracies or outdated information. Dispute any errors you find with the credit bureau to ensure your report reflects your true financial standing. An accurate credit report enhances your credibility as a borrower. It’s a simple yet effective way to boost your approval chances.

6. Maintain a Stable Income

Lenders favor applicants with a stable and reliable income. Ensure you have a consistent income stream before applying for Care Credit. If possible, increase your income through additional employment or freelance work. Providing proof of stable income can significantly improve your approval odds. It demonstrates your ability to repay the borrowed amount.

7. Keep Your Credit Utilization Low

Credit utilization refers to the percentage of your available credit that you are using. Aim to keep your utilization below 30% to improve your credit score. High utilization suggests you might be over-relying on credit, which can be a red flag for lenders. Paying down balances and increasing credit limits can help lower your utilization rate. A low utilization rate indicates responsible credit management.

8. Use a Co-Signer

If your credit score is not strong enough on its own, consider using a co-signer. A co-signer with a good credit history can enhance your approval odds. Ensure the co-signer understands their responsibility, as they will be liable for the debt if you default. This strategy can provide a safety net for both you and the lender. It’s a valuable option for those with limited credit history.

9. Build a Strong Credit History

A solid credit history will positively impact your Care Credit application. Use existing credit responsibly and make payments on time. Over time, a strong credit history will improve your score and approval odds. Avoid closing old credit accounts, as their history contributes to your credit profile. Consistent, positive credit behavior builds a trustworthy financial reputation.

10. Time Your Application Strategically

Timing can impact your Care Credit approval odds. Apply when your financial situation is stable, and your credit score is at its best. Avoid applying immediately after significant financial changes, such as job loss or large purchases. Strategic timing ensures you present the strongest possible application. It’s all about choosing the right moment to maximize your chances.

Boost Your Care Credit Approval Odds

Improving your Care Credit approval odds involves understanding the factors that influence your creditworthiness. By checking your credit score, managing debt, maintaining a stable income, and strategically timing your application, you can enhance your chances. Employing these tips and tricks ensures you are well-prepared for the Care Credit approval process. With careful planning and responsible financial behavior, you can achieve your healthcare financing goals.

Student loan debt is a significant financial challenge for millions of graduates. With the rising cost of education, more students are relying on loans to fund their college degrees, resulting in substantial debt upon graduation. This financial burden can impact various aspects of life, including the ability to save for retirement, purchase a home, or even pursue further education. The weight of student loans can also cause stress and anxiety, making it essential to find effective ways to manage and reduce this debt.

Student loan debt is a significant financial challenge for millions of graduates. With the rising cost of education, more students are relying on loans to fund their college degrees, resulting in substantial debt upon graduation. This financial burden can impact various aspects of life, including the ability to save for retirement, purchase a home, or even pursue further education. The weight of student loans can also cause stress and anxiety, making it essential to find effective ways to manage and reduce this debt.