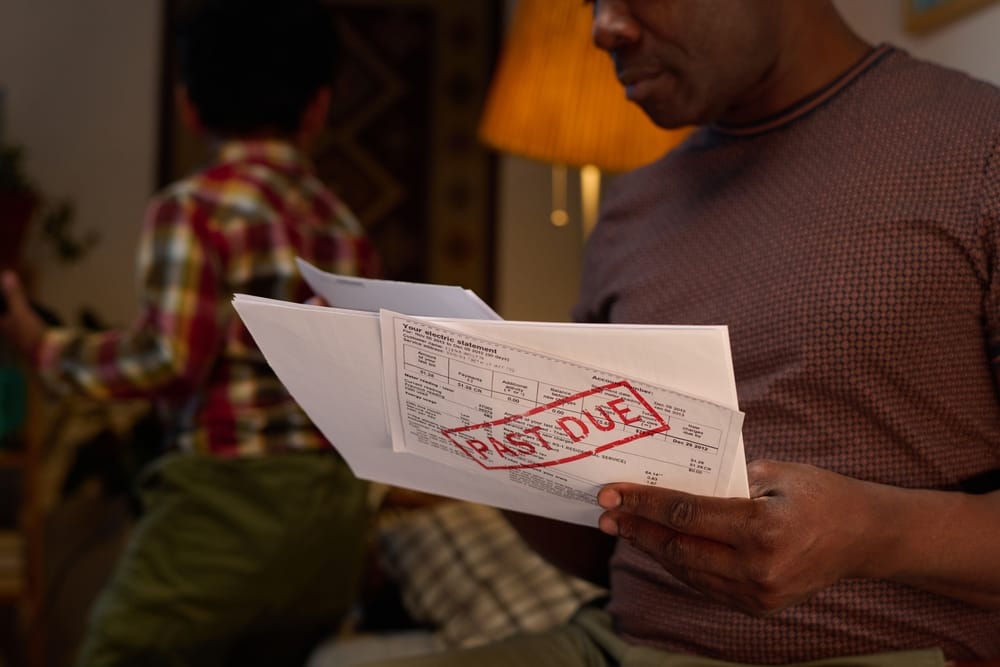

Tax season often brings hope for a refund, but joint filers now face an unexpected financial shock that catches many couples off guard. One spouse’s old debt can suddenly drain an entire refund before it ever hits a bank account. The IRS does not always send clear warnings before redirecting the money, which leaves couples scrambling for answers.

This issue affects everyday households, not just high-income earners or complex tax situations. Understanding how this process works helps prevent frustration and financial strain when filing jointly.

How One Spouse’s Debt Can Hijack a Joint Refund

Couples often choose joint filing to unlock tax benefits and simplify their paperwork, but this choice also ties both spouses to each other’s financial obligations. When one spouse owes back taxes, child support, or certain federal student loans, the Treasury Offset Program can step in. That program intercepts refunds and applies them directly to the debt without splitting responsibility. Many couples only discover the offset after checking their refund status and seeing a reduced or zero payout. This surprise creates tension because both partners expect equal access to the refund.

The IRS treats a joint refund as a single combined payment, not two separate shares, which creates complications when debt enters the picture. Even if only one spouse created the debt, the system can still apply the entire refund toward it. Some relief options exist, such as Innocent Spouse Relief, but those require separate filings and strict qualifications. Couples often miss these options because they do not receive clear upfront guidance during tax preparation. This structure leaves many families feeling blindsided during what should feel like a straightforward process.

Why the IRS Rarely Gives Advance Notice of Offsets

The IRS does not directly control all refund offsets, which surprises many taxpayers during filing season. Instead, other federal and state agencies notify the Treasury Offset Program when debts qualify for collection. Once that notification enters the system, the refund can get reduced or fully seized before any direct alert reaches the couple. This timing gap creates confusion because taxpayers often see the adjustment only after checking refund tools online. The lack of proactive communication makes the process feel abrupt and unpredictable.

Government agencies prioritize debt collection efficiency, which means refunds move quickly once flagged for offset. Notices often go to the debtor’s last known address, which may not reflect current living situations or shared household updates. Couples filing jointly rarely receive a combined warning that clearly explains the full impact on their refund. This communication gap leads to misunderstandings between spouses when money disappears unexpectedly. Financial experts often recommend checking debt status early in the tax season to reduce surprises.

Smart Ways Couples Can Protect Their Refund Before Filing

Couples can reduce risk by reviewing outstanding federal and state debts before submitting a joint tax return. Checking student loan status, unpaid taxes, and child support obligations helps reveal potential offsets early. Tax professionals often recommend using the IRS “Where’s My Refund” tool alongside the Treasury Offset Program contact line for added clarity. Couples who communicate openly about financial obligations often avoid last-minute shocks during refund season. Awareness creates more control over how and when a refund gets applied.

Filing separately sometimes helps protect one spouse’s portion of a refund, depending on income and deduction differences. However, separate filing can also reduce certain tax benefits, so couples need to weigh both outcomes carefully. Some spouses qualify for partial relief through IRS Form 8379, which helps injured spouses recover their share of a joint refund. Filing this form early improves the chance of receiving at least part of the refund back. Strategic planning before tax season often makes the biggest difference in avoiding financial loss.

What This Means for Joint Filers Moving Forward

Joint filing continues to offer tax advantages, but it also increases exposure to shared financial risks that many couples underestimate. One spouse’s debt can override expectations and reshape a household budget in seconds once the IRS processes an offset. Families who treat tax filing as a shared financial checkpoint often reduce surprises and improve long-term planning. Clear communication about debt and refund expectations strengthens financial stability during tax season. Couples who stay proactive gain more control over how their money moves through the system.

This issue highlights how important financial transparency becomes in shared tax decisions, especially when debts exist in either spouse’s name. Couples who ignore potential liabilities often face sudden disruptions that affect bills, savings, or planned expenses. Understanding how offsets work helps households prepare instead of reacting after money disappears. Tax season rewards preparation, not guesswork, and informed filers protect more of their refund. Staying alert to these rules keeps financial surprises from turning into financial setbacks.

What steps should couples take before filing jointly to avoid refund surprises like these?

You May Also Like…

Your Refund Could Be Redirected to State Debt Without a Single Notice From the IRS

Colorado TABOR Refunds Are Reduced When Residents Owe State Debts

Joint Tax Liability Rules Mean Spouses Can Still Owe Shared Tax Debts

11 Social Security Surprises That Hit You After Losing a Spouse

23% of Americans With Credit Card Debt Don’t Believe They’ll Ever Pay It Off

Brandon Marcus is a writer who has been sharing the written word since a very young age. His interests include sports, history, pop culture, and so much more. When he isn’t writing, he spends his time jogging, drinking coffee, or attempting to read a long book he may never complete.