The holidays are supposed to be magical—a time for twinkling lights, festive music, and, of course, gift-giving. But after the last present is unwrapped and the New Year’s confetti settles, reality often hits like a snowball to the face. Credit card statements arrive, debt balances loom, and suddenly, that cozy holiday cheer feels a lot more like financial panic. Even responsible spenders can fall into traps that quietly tank their credit score before January is over.

The problem is that holiday spending isn’t just about overspending—it’s about how small decisions compound in ways most people never anticipate.

1. Maxing Out Credit Cards Without A Repayment Plan

It’s tempting to swipe without thinking when stores are decked out in lights and promotions are everywhere. Unfortunately, maxing out your credit cards over the holidays can dramatically affect your credit utilization ratio, one of the most important factors in your score. High balances relative to your credit limit send a signal to lenders that you might be overextended. Even if you pay the balance off quickly, the timing of reporting can mean your January statement still shows a maxed-out card. Without a clear repayment plan, what felt like a festive splurge can quickly turn into a credit score nightmare.

2. Racking Up Multiple Store Credit Cards

Those “instant approval” offers at checkout might seem harmless—or even smart if they come with a discount. The reality is that opening multiple store credit cards in a short period can ding your credit score in multiple ways. Each application triggers a hard inquiry, which can shave points off your score temporarily. The added new accounts also reduce the average age of your credit history, another factor lenders evaluate. While one or two cards might be manageable, a stack of plastic can make January feel more stressful than celebratory.

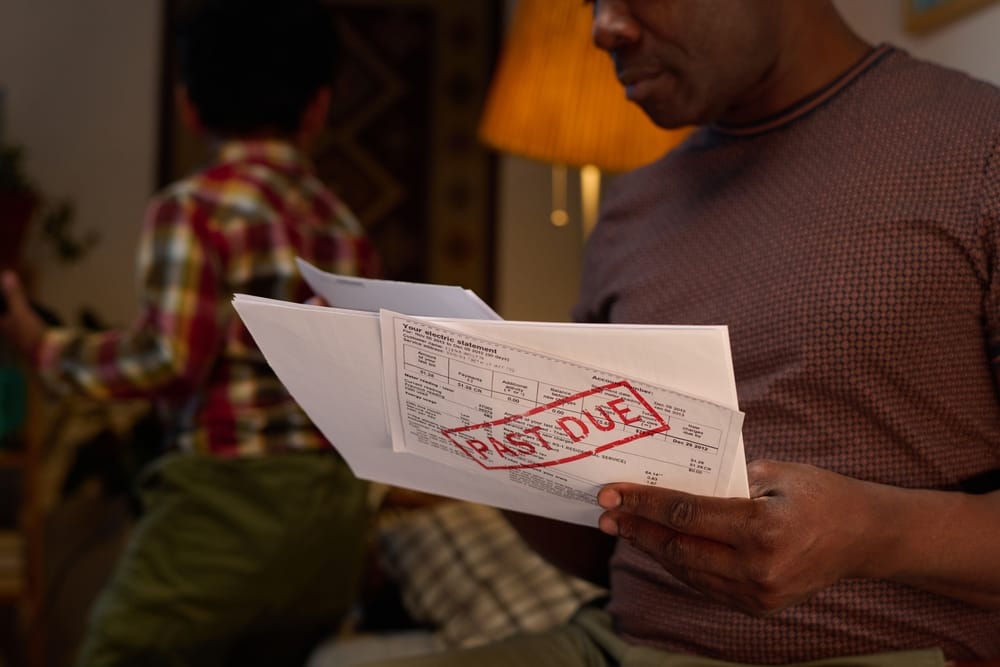

3. Missing Minimum Payments During Holiday Chaos

Holiday schedules are hectic, and bills can slip through the cracks. Missing a minimum payment—even by a few days—can have a surprisingly large impact on your credit score. Late payments are reported to credit bureaus and can linger on your report for years. The stress of managing gifts, parties, and travel often means people forget to prioritize monthly bills. Staying organized and setting reminders is critical; otherwise, that cheerful December spending spree can echo as a January credit disaster.

4. Overreliance On Buy Now, Pay Later Options

Buy Now, Pay Later (BNPL) services are everywhere, making it tempting to spread out payments over weeks or months. But while the idea feels harmless, these services can quietly affect your creditworthiness. Missing a payment or delaying your repayment can trigger late fees and potential credit reporting consequences. Even when you pay on time, juggling multiple BNPL plans can lead to a confusing financial picture that increases stress and risk. It’s easy to underestimate the impact until the first statement arrives in January—then panic sets in.

5. Ignoring Existing Debt When Holiday Shopping

It’s easy to get caught up in gift lists and holiday deals, but ignoring pre-existing debt can be dangerous. Adding new balances on top of old ones increases your total debt load and raises your credit utilization across all cards. Lenders see this as a higher risk, and your credit score can drop as a result. Even if your spending seems reasonable, failing to account for ongoing obligations can create a compounding effect. Keeping track of both old and new debt is essential to avoid a post-holiday financial hangover.

6. Not Monitoring Credit Reports Until It’s Too Late

After the holiday rush, many people don’t check their credit reports until something goes wrong. The problem is that errors, overlooked balances, or unexpected charges can silently damage your score if you’re not paying attention. Monitoring your credit allows you to catch issues early, dispute errors, and plan repayment strategies before they spiral. Waiting until January to see your credit score can be a rude awakening. Staying proactive during and after the holidays is key to preventing a financial headache you could have avoided.

Stay Ahead Of The Holiday Hangover

The holidays are meant to be joyful, but without careful planning, they can also trigger a credit score crisis that lasts well into the new year. From maxed-out cards to missed payments and Buy Now, Pay Later traps, even well-intentioned spending can have long-term consequences.

Awareness is the first step—recognizing how decisions made in December can affect January and beyond allows you to act before the damage is done. By planning, tracking, and staying organized, it’s possible to enjoy the season without financial regrets.

Have you ever experienced a post-holiday credit surprise? Share your stories, tips, or cautionary tales in the comments section below—we want to hear your experiences.

You May Also Like…

6 Credit Mistakes That Redditors Confess Cost Them Thousands

8 “Harmless” Daily Habits That Are Secretly Wrecking Your Credit Score

The Medical Bill Mistake That Can Cripple Your Credit for a Decade

Accelerate Your Debt Repayment Using Our Powerful Snowball Method.

6 Sneaky Financial Risks Hiding in Holiday Spending

Brandon Marcus is a writer who has been sharing the written word since a very young age. His interests include sports, history, pop culture, and so much more. When he isn’t writing, he spends his time jogging, drinking coffee, or attempting to read a long book he may never complete.