The 2027 Social Security COLA grabs attention because it signals a bigger boost in monthly benefits for millions of retirees. On paper, a higher COLA sounds like good news because it reflects rising wages and prices across the economy. Many seniors expect that increase to ease financial pressure, especially with everyday costs climbing at grocery stores and pharmacies. The reality tells a more complicated story once healthcare, housing, and taxes enter the equation. A larger benefit check does not always translate into stronger purchasing power.

Inflation drives the COLA calculation, and the government ties it to the Consumer Price Index for Urban Wage Earners and Clerical Workers. That index often reflects working-age spending patterns more than senior-specific costs. Retirees often spend more on healthcare and housing than the index fully captures. That mismatch sets up a situation where benefit increases lag behind real-life expenses. The 2027 COLA surge reflects inflation trends, not guaranteed financial relief.

COLA Looks Bigger, But Inflation Writes the Script

The Cost-of-Living Adjustment rises when inflation pushes prices higher across the economy. The Social Security Administration uses third-quarter CPI-W data to calculate the annual increase. A spike in energy, food, or housing costs can push the COLA upward quickly. That process makes the adjustment reactive rather than proactive. Seniors often see the increase as relief, but inflation often moves first.

A strong COLA year often signals that prices already climbed significantly. Grocery bills, utility costs, and rent usually increase before benefit checks adjust. That timing gap creates frustration for retirees on fixed incomes. A higher COLA does not reverse past price increases. It only tries to catch up with them.

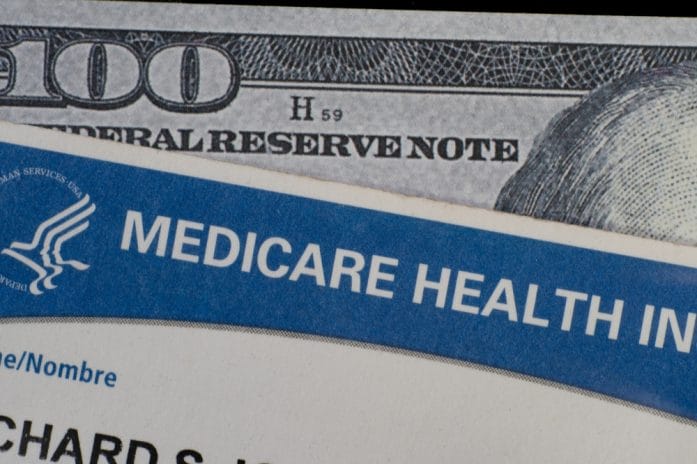

Medicare Premiums Take a Big Bite First

Medicare Part B premiums often rise alongside or even faster than Social Security benefits. Seniors automatically see those premiums deducted from monthly checks. That deduction reduces the net impact of any COLA increase. Even a strong COLA can shrink quickly once healthcare costs enter the equation. Many retirees notice smaller-than-expected deposits because of this shift.

Medical expenses continue to rise due to higher service costs and prescription prices. Seniors often rely heavily on healthcare services, which increases exposure to those price jumps. Supplemental plans and out-of-pocket costs also add pressure. The healthcare system pulls more from benefit increases each year. That reality often offsets COLA gains before they reach daily budgets.

Taxes and Income Thresholds Add More Pressure

Social Security benefits can face federal income taxes when total income crosses certain thresholds. A larger COLA can push more retirees into taxable territory. That shift reduces the net benefit increase even further. Some states also tax Social Security income, which adds another layer of cost. Retirees often overlook this effect until tax season arrives.

Income-related Medicare adjustments, known as IRMAA surcharges, also increase with higher reported income. Those surcharges apply to higher-income retirees enrolled in Medicare. Even modest benefit increases can trigger higher premiums under these rules. That structure creates a hidden penalty for COLA growth. Many seniors feel like raises disappear before they reach daily spending.

The CPI Gap Leaves Seniors Behind Real Costs

The COLA calculation relies on CPI-W, but many experts argue that CPI-E better reflects senior spending patterns. CPI-E focuses more on healthcare and housing, which dominate retirement budgets. Those categories often rise faster than the general inflation index. That gap causes Social Security adjustments to lag behind real expenses. Seniors feel that difference most strongly during high-inflation periods.

Housing costs continue to rise across many regions, including rent and property taxes. Seniors who rent often face annual increases that exceed COLA gains. Homeowners also deal with maintenance, insurance, and tax hikes. The CPI-W does not fully capture those pressures. That mismatch keeps retirement budgets tight even during COLA growth years.

The Right Moves That Help Stretch Every COLA Dollar

Budget adjustments become essential when benefit increases fail to match expenses. Seniors often benefit from reviewing subscription costs, insurance plans, and utility usage. Small changes in spending habits can free up meaningful monthly cash flow. Local assistance programs also help reduce food and healthcare costs. Strategic planning makes a noticeable difference over time.

Delaying certain expenses or switching providers can also improve financial stability. Prescription discount programs and Medicare savings plans reduce out-of-pocket pressure. Some retirees also explore part-time work to supplement income without losing benefits. Careful planning helps offset the gap between COLA increases and real-world inflation. Strong financial habits matter more during high-cost years.

Why a Bigger COLA Does Not Guarantee Relief

A rising COLA signals economic pressure, not financial comfort for retirees. Inflation, healthcare costs, taxes, and housing expenses all compete against benefit increases. Seniors often feel the increase in their checks disappear quickly after deductions and price hikes. The system adjusts benefits annually, but costs change month by month. That timing gap shapes the real impact of the 2027 COLA surge.

What do you think matters more right now—higher COLA increases or stronger controls on healthcare and housing costs? Let’s hear your thoughts and experiences in the comments below.

You May Also Like…

The Medicare Premium Increase That Could Consume Nearly One-Third of Some Retirees’ COLA Boost

5 Ways Hackers Can Steal Your Social Security Check With Your Help

The 2027 Social Security COLA Forecast Just Jumped — Here’s What Could Still Reduce Your Check

Michigan Seniors Are Delaying Downsizing as Mortgage Rates and Insurance Costs Stay Elevated

Brandon Marcus is a writer who has been sharing the written word since a very young age. His interests include sports, history, pop culture, and so much more. When he isn’t writing, he spends his time jogging, drinking coffee, or attempting to read a long book he may never complete.