The price of living somewhere no longer stops at rent or a mortgage. Insurance has stepped into the spotlight, and it refuses to stay quiet. Premiums have surged across the country, and in some places, they have exploded so dramatically that entire communities now sit on the edge of affordability. Homeowners who once felt secure now scan renewal notices with a mix of disbelief and dread, wondering how a bill tied to “protection” turned into a dealbreaker. The map of where people can live comfortably has started to shift, and insurance companies now hold more influence over that map than many ever expected.

Coastal dream homes, wildfire-adjacent retreats, and even suburban neighborhoods that once felt like safe bets now carry price tags that extend far beyond the purchase price. Insurance costs don’t just reflect risk anymore; they actively shape decisions about where families settle, where retirees relocate, and where younger buyers even dare to look.

When “Affordable” Stops Meaning What It Used To

For decades, affordability centered on a simple equation: income, mortgage, and maybe property taxes. That formula now looks outdated. Insurance premiums have surged in many regions, especially in areas prone to hurricanes, wildfires, flooding, and severe storms. States like Florida and California have become headline examples, where some homeowners have seen premiums double or even triple in a short period. That kind of increase doesn’t just sting; it completely reshapes budgets and forces tough decisions about staying put or moving on.

Insurance companies have tightened their grip on risk, and they no longer hesitate to pull back from areas they consider too volatile. Some insurers have stopped writing new policies in high-risk regions altogether, leaving homeowners scrambling for limited and often expensive alternatives. This shrinking pool of options drives prices even higher, creating a cycle that feels impossible to escape. Homebuyers now factor insurance quotes into their decision-making process before they even make an offer, because ignoring it could mean walking into a financial trap.

That reality forces a mindset shift. Buyers who once chased ocean views or wooded privacy now look for “insurability” as a key feature. A home that looks perfect on paper can quickly lose its shine when the insurance estimate arrives. People have started asking different questions: How close is the nearest fire station? Has this area seen recent claims? What do insurers say about future risk? Those questions now shape the housing search just as much as square footage or school districts.

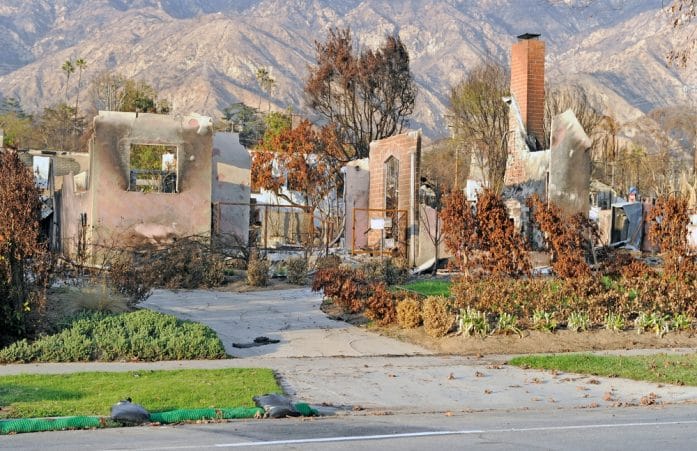

The Climate Factor Nobody Can Ignore Anymore

Climate risk has moved from an abstract concept to a daily reality, and insurance companies have responded with sharp adjustments. Wildfires in the West, hurricanes along the Gulf and East Coasts, and floods in unexpected regions have driven massive payouts for insurers. Those losses don’t disappear; companies pass them along through higher premiums or stricter coverage terms. The result lands squarely on homeowners’ shoulders, and it often arrives faster than expected.

Insurers rely on advanced data models that predict future risk, not just past events. That forward-looking approach means areas that haven’t yet faced a major disaster can still see rising premiums if models suggest trouble ahead. Homeowners sometimes feel blindsided when their rates jump without a recent claim, but insurers have already factored in shifting weather patterns and increasing disaster frequency. This disconnect between personal experience and projected risk creates frustration, especially when costs climb without a clear, visible cause.

The Ripple Effect on Housing Markets

Rising insurance costs don’t stay confined to monthly bills; they ripple through entire housing markets. When insurance becomes too expensive, demand in certain areas begins to cool, and that shift can slow price growth or even push values downward. Sellers in high-risk regions now face an additional challenge, because buyers factor insurance costs into their overall budget and often walk away from deals that no longer make financial sense. What once looked like a hot market can lose momentum quickly when insurance enters the equation.

Lenders have also taken notice. Mortgage approvals often depend on proof of adequate insurance coverage, and when policies become difficult to obtain or prohibitively expensive, financing can fall through. That reality adds another layer of complexity for buyers, who must navigate not just interest rates and home prices but also insurance availability. A home that qualifies for a loan one year might become harder to finance the next, simply because insurance conditions changed.

This dynamic has started to influence migration patterns in subtle but significant ways. Some people leave high-cost, high-risk areas for regions with more stable insurance markets, even if it means sacrificing certain lifestyle perks. Others stay put but adjust expectations, opting for smaller homes or different neighborhoods to offset rising premiums. The housing market doesn’t just reflect personal preferences anymore; it reflects a growing awareness of long-term risk and financial sustainability.

Strategies for Staying Ahead of the Insurance Squeeze

Navigating this new landscape requires a proactive approach, because waiting for renewal notices can lead to unpleasant surprises. Homeowners benefit from shopping around for insurance regularly, even if they feel satisfied with their current provider. Different companies assess risk differently, and comparing quotes can reveal opportunities to save or find better coverage. Loyalty doesn’t always pay in this market, so staying informed matters more than ever.

Bundling policies, increasing deductibles, and asking about discounts for safety upgrades can also help manage costs. Insurers often reward homeowners who take steps to reduce risk, and those incentives can add up over time. Installing security systems, reinforcing roofs, or upgrading electrical systems can make a property more appealing from an insurance perspective. These improvements require upfront investment, but they can lead to long-term savings and greater peace of mind.

Location research has become a critical step for anyone considering a move. Checking local insurance trends, understanding regional risks, and reviewing state-backed insurance options can provide valuable insight before making a decision. Some states offer last-resort insurance programs for high-risk areas, but those policies often come with higher costs and limited coverage. Knowing these details ahead of time helps avoid surprises and allows for smarter planning. A little homework now can prevent major financial headaches later.

The New Geography of Affordability

A new map has started to emerge, and it doesn’t look like the one people grew up with. Insurance costs have quietly redrawn the boundaries of affordability, turning some once-desirable locations into financial challenges while elevating others as safer bets. This shift doesn’t mean people will abandon entire regions overnight, but it does mean decisions about where to live now carry more weight and complexity than ever before. Housing choices have become deeply intertwined with risk, resilience, and long-term cost planning.

What changes feel most realistic right now—adjusting expectations, relocating, or investing in upgrades to stay put? Drop your thoughts, strategies, or even frustrations in the comments and keep the conversation going.

You May Also Like…

7 Reasons Your Home Insurance Premium Just Went Up Again

8 Super Simple Ways to Reduce Your Car Insurance Premiums

Your House Is Holding You Back: Why So Many People Are Re‑Thinking Homeownership

Colorado Escrow Payments Continue Climbing — Homeowners Face Higher Monthly Costs

Avoid These Pitfalls: First-Time Homeownership Mistakes That Can Cost You

Brandon Marcus is a writer who has been sharing the written word since a very young age. His interests include sports, history, pop culture, and so much more. When he isn’t writing, he spends his time jogging, drinking coffee, or attempting to read a long book he may never complete.