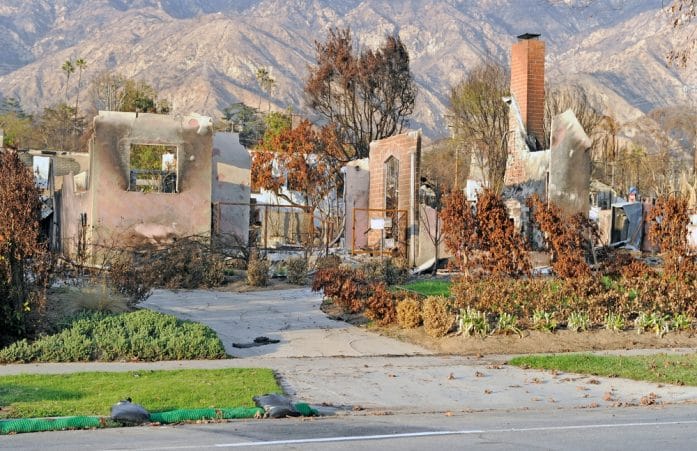

Texas property insurance costs jumped sharply last year, shaking up retirement budgets across the state. Some counties reported premium increases topping 20%, creating immediate strain for homeowners on fixed incomes. Rising storm risks, higher reconstruction costs, and surging reinsurance prices all pushed insurers to raise rates. Many retirees who planned carefully for retirement now face unexpected financial pressure that disrupts monthly stability. A typical homeowner in hard-hit areas now pays hundreds more per year just to maintain basic coverage.

Retirees across coastal and storm-prone regions feel the pressure the most, especially those living on Social Security and modest pensions. Insurance bills now compete directly with essentials like groceries, utilities, and medication. Some seniors report opening renewal letters with shock after years of steady or predictable rates. A retiree in South Texas, for example, may now pay significantly more than just two years ago for the same coverage level. Financial planners warn that this trend could reshape retirement security in high-risk states like Texas.

The Everyday Cuts Retirees Are Making to Stay Afloat

Rising insurance premiums force many Texas retirees to make immediate lifestyle adjustments. Grocery budgets shrink as seniors swap fresh produce and protein-heavy items for cheaper pantry staples. Utility usage drops as households carefully track air conditioning and heating to control monthly bills. Some retirees pause home maintenance projects, delaying roof repairs or landscaping work to preserve cash flow. Even small expenses like streaming services or community club memberships disappear from monthly budgets.

Transportation habits also shift as retirees reduce driving to save on gas and vehicle maintenance. Many seniors now cluster errands into single trips instead of multiple weekly outings. Dining out becomes rare, reserved only for special occasions rather than routine social activity. Emergency savings accounts shrink as insurance premiums consume a larger share of fixed income. These daily trade-offs reveal how sharply housing-related costs ripple through every part of retirement life.

Why Texas Premiums Keep Climbing Faster Than Inflation

Insurance companies in Texas face mounting pressure from repeated severe weather events, including hurricanes, hailstorms, and flooding. These disasters increase claim payouts and push insurers to rebuild financial reserves more aggressively. Reinsurance costs, which insurers pay to protect themselves, also rise quickly as global disaster risks grow. Construction costs in Texas continue to climb, making home repairs and rebuilding significantly more expensive after storms. These combined pressures force insurers to adjust premiums faster than general inflation rates.

Population growth in high-risk regions adds another layer of complexity to pricing models. More homes in storm-prone zones increase the total exposure insurers must cover. Fraud prevention costs and legal expenses also rise, contributing to higher overall operational costs. Regulators attempt to balance affordability with insurer stability, but market realities often dominate pricing decisions. Texas homeowners now experience a market where risk and cost increasingly shape every renewal notice.

Smart Ways Seniors Are Fighting Back Against Rising Costs

Some Texas retirees actively shop around for new insurance providers to find better rates. Comparison shopping often reveals significant differences between carriers for nearly identical coverage. Bundling home and auto insurance policies sometimes unlocks meaningful discounts for fixed-income households. Higher deductibles also lower monthly premiums, though this strategy requires careful risk planning. Seniors increasingly consult independent insurance brokers to navigate complex policy options.

Home upgrades also play a major role in lowering premiums over time. Impact-resistant roofs, storm shutters, and updated plumbing systems can reduce risk profiles in the eyes of insurers. Some counties even offer mitigation grants that help retirees fund these improvements. Community groups and senior organizations provide education sessions on cost-saving insurance strategies. These proactive steps help retirees regain some control over rising housing expenses.

What This Means for Texas Retirement Security Moving Forward

Texas retirement security now faces a growing challenge as housing costs consume a larger share of fixed incomes. Insurance premiums alone now rival property tax increases in their impact on monthly budgets. Seniors who planned retirement around stable housing expenses now rethink long-term financial strategies. Some retirees consider downsizing or relocating to lower-risk areas to stabilize costs. Financial advisors emphasize that housing affordability now sits at the center of retirement planning discussions.

How should retirees balance rising home protection costs with the need to preserve financial stability in retirement? We want your advice, experiences, and stories shared below in our comments section.

You May Also Like…

Why Some Banks Are Tightening Cash Access in Texas and Florida

Wyoming Property Tax Relief Deadline: Missing the May Filing Window Can Cost Homeowners Thousands

Nevada Trust Rules Offer Less Asset Protection Than Many Homeowners Expect

What Are New Jersey’s ANCHOR Rebate Payments And How Can They Help Homeowners?

Florida Homeowners Are Seeing Major Premium Increases as Citizens Policies Adjust Rates

Brandon Marcus is a writer who has been sharing the written word since a very young age. His interests include sports, history, pop culture, and so much more. When he isn’t writing, he spends his time jogging, drinking coffee, or attempting to read a long book he may never complete.